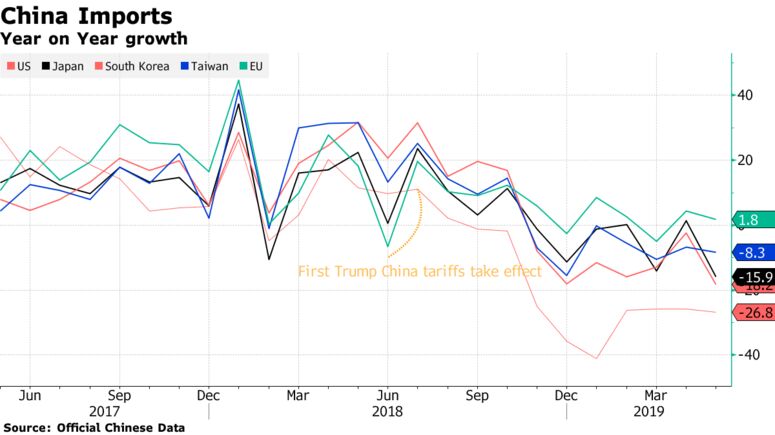

A trade war between the world's two largest economies erupted this year, and technology is at the center of the skirmish. President Donald Trump blocked networking giant Huawei Technologies Co. from buying U.S. components, and put tariffs on many Chinese products. China responded by threatening to blacklist U.S. companies. The rising tension is testing a complex relationship, especially in tech where the U.S. and China are tightly intertwined through global supply chains and software that can zip across borders with the tap of a computer key. So which country has the most to lose? Who needs the other nation more?

Computer Chips

China's greatest reliance on the U.S. is arguably in semiconductors.

China's semiconductor imports surge

U.S. companies Intel Corp. and Nvidia Corp. dominate the market for processors, the key component of all laptops, desktop and server computers. The only viable alternative is another American firm: Advanced Micro Devices Inc.

Global computer chips market share, 2017

The three companies are based a short walk from each other in Silicon Valley, where they design their products.

A few Huawei U.S. locations situated near other chip-making companies

The processors are manufactured mostly in Taiwan. Intel has one plant in China, but it makes memory chips—a commodity component. Huawei unveiled its first home-grown server chip this year, based on designs from ARM Holdings Inc., which is headquartered in the U.K. ARM has operations in the U.S., too, and the company recently said its products fall under the U.S. export controls. Without the latest ARM designs, Huawei may struggle to make its own chips.

CRUCIAL NEEDS

Mobile Chips

In smartphones, Huawei is more independent, supplying at least two-thirds of its own processors and modems, according to analysts' estimates.

Percentage of Huawei's phones

using its own chips, 2018

But other Chinese smartphone makers, such as Xiaomi, Vivo, Oppo and Lenovo, rely much more on San Diego, California-based Qualcomm Inc., the world's largest mobile chip maker.

CRUCIAL NEEDS

Switch Chips

Switch chips run machines that direct the flow of information across computer networks including the internet. This is another area of technology where China relies on the U.S. Broadcom Inc., headquartered in San Jose, California, is the largest maker of switch chips.

Ethernet switch chips market share, 2018

Huawei, a top networking gear provider, has been a huge buyer of these components. If the Chinese company wanted to develop its own switch chips, it would still need other U.S. technology. Synopsys Inc. and Cadence Design Systems Inc. are the main suppliers of software that's used to design chips—and they both cut Huawei off recently.

Internet Switches Market share

by shipments, 2018 Q4

TAKE IT OR LEAVE IT

Microsoft

Microsoft's Windows operating system still runs most personal computers, including almost all the PCs China buys. Windows is still used by the Chinese government and government-owned entities. Microsoft's Office productivity software is also popular in the country.

Desktop operating system market share, May 2019

Microsoft hasn't said whether it can keep supplying Windows and Office to Huawei and other Chinese technology companies.

Worldwide PC shipments market share, Q1 2019

A prolonged ban on the supply of Windows and Office to Chinese computer makers would force them to build alternatives that don't exist yet. Lenovo, the world's biggest PC manufacturer, is Microsoft's biggest customer, according to Bloomberg supply-chain analysis.

TAKE IT OR LEAVE IT

Apple

Chinese consumers are increasingly embracing alternatives to the iPhone as Apple's devices have become more expensive and local smartphones have improved.

Handset shipments by phone type

Huawei has gone from a small smartphone player to overtaking Apple, mainly on the strength of demand in China—a surge also felt by other local phone makers Xiaomi, Oppo and Vivo.

China smartphone market share by shipments

In China, Apple offers some services like Apple Music, but newer products—the forthcoming Apple credit card, Apple News+, and Apple TV+—either won't launch in China or won't be immediately available there. Chinese consumers have already embraced local alternatives. Tencent Music's monthly user count easily exceeds the total population of the U.S.

Mobile active users for Tencent Music

The main reason China needs Apple is jobs. The U.S. tech giant has most of its devices made in China, supporting about 3 million workers there.

Apple supplier facilities by country, 2019

TAKE IT OR LEAVE IT

Mobile Software

Google's Android smartphone operating system is ubiquitous in the country, running on phones from Huawei, Oppo, Vivo and Lenovo. But for Chinese consumers, these manufacturers use a skeletal version of the software that has no Google services.

Global smartphone shipments using

Android operating system, by company

Outside China, they still need Google's support, though. When the U.S. internet giant recently said it would cut off Huawei's access to the full Android software, that was a major setback.

Smartphone shipments by OS, 2018

TAKE IT OR LEAVE IT

Artificial Intelligence

China is betting heavily on AI. Money is pouring in from China's investors, big internet companies and its government, driven by a belief that the technology can remake entire sectors of the economy, as well as national security. A similar effort is underway in the U.S., but in this new global arms race, China has three advantages: A vast pool of engineers to write the software, a massive base of 751 million internet users to test it on, and most importantly staunch government support that includes handing over gobs of citizens' data—something that makes Western officials squirm.

AI startups by most equity funding raised,

as of June 21, 2019

WHO NEEDS IT?

Cloud Services

Amazon.com Inc., Microsoft Corp. and Google are the biggest U.S. providers of computing power and services over the internet.

Amazon cloud revenue projection

But in China, the companies don't even make the top six. Alibaba Group Holding Ltd., Tencent Holdings Ltd. and their compatriots dominate the domestic market, and they're on the rise in other parts of the Asia Pacific region, according to Synergy Research Group.

Chinese companies' share of

cloud market in APAC, Q1 2019

WHO NEEDS IT?

Online Search

Baidu runs the largest search engine in China. Google pulled out of the country in 2010 and recent efforts to return have failed so far.

Top search engines, unique visitors

WHO NEEDS IT?

Online Shopping

Chinese consumers don't need U.S. companies for their online shopping needs. Amazon plans to shut down its Chinese marketplace business in July, and will only sell goods to mainland customers seeking products from other countries.

Alibaba and JD.com dominate the market, and Amazon never reached more than 1% market share, according to iResearch.

WHO NEEDS IT?

Social Networks

American social networks also aren't a part of daily life in China. Facebook Inc. and Twitter Inc. don't operate there—and that's not likely to change any time soon.

WeChat, the messaging service owned by Tencent, is China's leading hub for communication and other everyday tasks, like making mobile payments.

That's about 673M

more than the 2018

U.S. population

QQ, another messaging service also owned by Tencent and popular with younger internet users, has 823 million monthly users.

QQ monthly active users, March 2019

That's about

1/10th of the

global population

Weibo, a Chinese social network similar to Twitter, has more than 203 million daily active users—almost 70 million more than Twitter has.

Weibo and Twitter monthly active users

Sources:

- Computer chips: General Administration of Customs, PRC, IDC, Google Earth, Huawei Technologies Co.

- Mobile chips: Stifel Nicolaus, Bloomberg

- Switch chips: The Linley Group, IDC

- Microsoft: NetApplications.com, IDC, Imaginechina via AP Images

- Apple: IDC, Tencent Music Entertainment Group, Apple Company Filings

- Online search: iResearch, Bloomberg

- Mobile Software: IDC

- Artificial Intelligence: Pitchbook

- Cloud services: Bloomberg Intelligence, Synergy Research

- Online shopping: Amazon/company filings, eMarketer

- Social network: VCG/VCG via Getty Images, WeChat, U.S. Census Bureau, Tencent, Company Filings, Bloomberg

Additional work by: Lulu Chen, Edwin Chan and Matt Turner

Editor: Alistair BarrBy Ian King, Mira Rojanasakul and Adrian Leung

A trade war between the world's two largest economies erupted this year, and technology is at the center of the skirmish. President Donald Trump blocked networking giant Huawei Technologies Co. from buying U.S. components, and put tariffs on many Chinese products. China responded by threatening to blacklist U.S. companies. The rising tension is testing a complex relationship, especially in tech where the U.S. and China are tightly intertwined through global supply chains and software that can zip across borders with the tap of a computer key. So which country has the most to lose? Who needs the other nation more?

CRUCIAL NEEDS

Computer Chips

China's greatest reliance on the U.S. is arguably in semiconductors.

China's semiconductor imports surge

U.S. companies Intel Corp. and Nvidia Corp. dominate the market for processors, the key component of all laptops, desktop and server computers. The only viable alternative is another American firm: Advanced Micro Devices Inc.

Global computer chips market share, 2017

The three companies are based a short walk from each other in Silicon Valley, where they design their products.

A few Huawei U.S. locations situated near other chip-making companies

The processors are manufactured mostly in Taiwan. Intel has one plant in China, but it makes memory chips—a commodity component. Huawei unveiled its first home-grown server chip this year, based on designs from ARM Holdings Inc., which is headquartered in the U.K. ARM has operations in the U.S., too, and the company recently said its products fall under the U.S. export controls. Without the latest ARM designs, Huawei may struggle to make its own chips.

CRUCIAL NEEDS

Mobile Chips

In smartphones, Huawei is more independent, supplying at least two-thirds of its own processors and modems, according to analysts' estimates.

Percentage of Huawei's phones

using its own chips, 2018

But other Chinese smartphone makers, such as Xiaomi, Vivo, Oppo and Lenovo, rely much more on San Diego, California-based Qualcomm Inc., the world's largest mobile chip maker.

CRUCIAL NEEDS

Switch Chips

Switch chips run machines that direct the flow of information across computer networks including the internet. This is another area of technology where China relies on the U.S. Broadcom Inc., headquartered in San Jose, California, is the largest maker of switch chips.

Ethernet switch chips market share, 2018

Huawei, a top networking gear provider, has been a huge buyer of these components. If the Chinese company wanted to develop its own switch chips, it would still need other U.S. technology. Synopsys Inc. and Cadence Design Systems Inc. are the main suppliers of software that's used to design chips—and they both cut Huawei off recently.

Internet Switches Market share

by shipments, 2018 Q4

TAKE IT OR LEAVE IT

Microsoft

Microsoft's Windows operating system still runs most personal computers, including almost all the PCs China buys. Windows is still used by the Chinese government and government-owned entities. Microsoft's Office productivity software is also popular in the country.

Desktop operating system market share, May 2019

Microsoft hasn't said whether it can keep supplying Windows and Office to Huawei and other Chinese technology companies.

Worldwide PC shipments market share, Q1 2019

A prolonged ban on the supply of Windows and Office to Chinese computer makers would force them to build alternatives that don't exist yet. Lenovo, the world's biggest PC manufacturer, is Microsoft's biggest customer, according to Bloomberg supply-chain analysis.

TAKE IT OR LEAVE IT

Apple

Chinese consumers are increasingly embracing alternatives to the iPhone as Apple's devices have become more expensive and local smartphones have improved.

Handset shipments by phone type

Huawei has gone from a small smartphone player to overtaking Apple, mainly on the strength of demand in China—a surge also felt by other local phone makers Xiaomi, Oppo and Vivo.

China smartphone market share by shipments

In China, Apple offers some services like Apple Music, but newer products—the forthcoming Apple credit card, Apple News+, and Apple TV+—either won't launch in China or won't be immediately available there. Chinese consumers have already embraced local alternatives. Tencent Music's monthly user count easily exceeds the total population of the U.S.

Mobile active users for Tencent Music

The main reason China needs Apple is jobs. The U.S. tech giant has most of its devices made in China, supporting about 3 million workers there.

Apple supplier facilities by country, 2019

TAKE IT OR LEAVE IT

Mobile Software

Google's Android smartphone operating system is ubiquitous in the country, running on phones from Huawei, Oppo, Vivo and Lenovo. But for Chinese consumers, these manufacturers use a skeletal version of the software that has no Google services.

Global smartphone shipments using

Android operating system, by company

Outside China, they still need Google's support, though. When the U.S. internet giant recently said it would cut off Huawei's access to the full Android software, that was a major setback.

Smartphone shipments by OS, 2018

TAKE IT OR LEAVE IT

Artificial Intelligence

China is betting heavily on AI. Money is pouring in from China's investors, big internet companies and its government, driven by a belief that the technology can remake entire sectors of the economy, as well as national security. A similar effort is underway in the U.S., but in this new global arms race, China has three advantages: A vast pool of engineers to write the software, a massive base of 751 million internet users to test it on, and most importantly staunch government support that includes handing over gobs of citizens' data—something that makes Western officials squirm.

AI startups by most equity funding raised,

as of June 21, 2019

WHO NEEDS IT?

Cloud Services

Amazon.com Inc., Microsoft Corp. and Google are the biggest U.S. providers of computing power and services over the internet.

Amazon cloud revenue projection

But in China, the companies don't even make the top six. Alibaba Group Holding Ltd., Tencent Holdings Ltd. and their compatriots dominate the domestic market, and they're on the rise in other parts of the Asia Pacific region, according to Synergy Research Group.

Chinese companies' share of

cloud market in APAC, Q1 2019

WHO NEEDS IT?

Online Search

Baidu runs the largest search engine in China. Google pulled out of the country in 2010 and recent efforts to return have failed so far.

Top search engines, unique visitors

WHO NEEDS IT?

Online Shopping

Chinese consumers don't need U.S. companies for their online shopping needs. Amazon plans to shut down its Chinese marketplace business in July, and will only sell goods to mainland customers seeking products from other countries.

Alibaba and JD.com dominate the market, and Amazon never reached more than 1% market share, according to iResearch.

WHO NEEDS IT?

Social Networks

American social networks also aren't a part of daily life in China. Facebook Inc. and Twitter Inc. don't operate there—and that's not likely to change any time soon.

WeChat, the messaging service owned by Tencent, is China's leading hub for communication and other everyday tasks, like making mobile payments.

That's about 673M

more than the 2018

U.S. population

QQ, another messaging service also owned by Tencent and popular with younger internet users, has 823 million monthly users.

QQ monthly active users, March 2019

That's about

1/10th of the

global population

Weibo, a Chinese social network similar to Twitter, has more than 203 million daily active users—almost 70 million more than Twitter has.

Weibo and Twitter monthly active users

Sources:

- Computer chips: General Administration of Customs, PRC, IDC, Google Earth, Huawei Technologies Co.

- Mobile chips: Stifel Nicolaus, Bloomberg

- Switch chips: The Linley Group, IDC

- Microsoft: NetApplications.com, IDC, Imaginechina via AP Images

- Apple: IDC, Tencent Music Entertainment Group, Apple Company Filings

- Online search: iResearch, Bloomberg

- Mobile Software: IDC

- Artificial Intelligence: Pitchbook

- Cloud services: Bloomberg Intelligence, Synergy Research

- Online shopping: Amazon/company filings, eMarketer

- Social network: VCG/VCG via Getty Images, WeChat, U.S. Census Bureau, Tencent, Company Filings, Bloomberg

Additional work by: Lulu Chen, Edwin Chan and Matt Turner

Editor: Alistair Barr

-- via my feedly newsfeed