Saturday, May 23, 2026

Monday, September 1, 2025

Consequences of Trump, or something more fundamental?

via Bloomberg -- excerpted from "Balance of Power" email from David Westin.

Welcome to Balance of Power, bringing you the latest in global politics. If you haven’t yet, sign up here.

Chinese leader Xi Jinping and Russian President Vladimir Putin have long showcased their bromance on the world stage.

Now, they’re embracing a powerful new friend: Indian Prime Minister Narendra Modi.

Pictures of the three leaders laughing during an impromptu huddle today on the sidelines of the Shanghai Cooperation Organisation summit in the Chinese city of Tianjin signaled the beginning of a new chapter in regional diplomacy.

Putin, Modi and Xi at the SCO summit. Source: Kyodo News/Getty Images

“Exchanging perspectives with President Putin and President Xi during the SCO Summit,” Modi posted on his official X account.

For Xi, the optics could hardly have been better. As US President Donald Trump’s tariffs and foreign-policy swings upend America’s global standing, China’s leader is seeking to elevate Beijing’s position on the world stage.

Making up with Modi is part of that push.

It’s just two years ago that Xi broke decades of precedent to skip a Group of 20 summit in New Delhi, dealing a public snub to Modi as tensions simmered between the world’s two most populous nations.

Now, with the US targeting Indian and Chinese exports with tariffs past 50%, the neighbors are putting aside their border dispute and eyeing ways to do more business.

And while Putin and Modi have long been partners — Russia is India’s primary defense supplier, after all — the three men together forging such a united front stands out.

That show of common purpose calls into question how effective Trump’s campaign to prise India away from Russian oil, and convince China to buy more from the US, is really going to be.

The answer may come only when Trump arrives in Beijing for his own taste of Xi’s diplomatic charm — the date for which still hasn’t been set.

For the time being, the emergence of a new Xi-Putin-Modi alliance is a worrying development for defenders of the US-led global order. — Jenni Marsh

Xi displayed on a screen at the SCO summit media center. Photographer: Qilai Shen/Bloomberg

Tuesday, August 26, 2025

Where Is the Global Resistance to Trump?

via Project Syndicate:

Aug 8, 2025

DANI RODRIK

US President Donald Trump’s reckless, self-destructive tariffs have given Europe, China, and various middle powers an opportunity to make a statement about who they are and what they stand for. With few exceptions, their responses have left much to be desired.

CAMBRIDGE – America’s critics have always depicted it as a selfish country that throws its weight around with little regard for others’ well-being. But President Donald Trump’s trade policies have been so misguided, erratic, and self-defeating as to make even the most cartoonish of such descriptions seem flattering. Still, in a twisted way, his trade follies have laid bare other countries’ failures as well, by forcing them to consider what their responses say about their own intentions and capabilities.

It is said that one’s true character is revealed in the face of adversity, and the same goes for countries and their political systems. Trump’s frontal assault on the world economy was a shock to everyone, but it also gave Europe, China, and various middle powers an opportunity to make a statement about who they are and what they stand for. It was an invitation to articulate a vision of a new world order that could overcome the imbalances, inequities, and unsustainability of the old one, and that would not depend on the leadership – for better or worse – of a single powerful country. But few rose to the challenge.

In this respect, the European Union has perhaps been the greatest disappointment. In terms of purchasing power, it is almost as large as the United States – accounting for 14.1% of the world economy, compared to 14.8% for the US and 19.7% for China. Moreover, despite the recent rise of the far right, most European countries have avoided backsliding into authoritarianism. As a collection of democratic nation-states whose geopolitical ambitions do not threaten others, Europe has both the power and the moral authority to provide global leadership. Instead, it dithered and then submitted to Trump’s demands.

Europe’s ambitions were always narrowly parochial; but in folding to Trump, it is not even clear that it served its own immediate interests. The July handshake deal between Trump and European Commission President Ursula von der Leyen leaves 50% tariffs on European exports of steel and aluminum, places 15% tariffs on most other exports, and commits Europe to ridiculously high levels of energy imports from the US. Rarely has the EU’s structural weakness as a confederation of countries without a collective sense of identity been on starker display.

China has played a tougher game, retaliating forcefully with its own tariffs and restricting exports of critical minerals to the US. Trump’s vindictive, self-defeating foreign policies have helped China extend its influence and enhance its credibility as a reliable partner for the developing world. But the Chinese leadership has also failed to articulate a practical model for a post-neoliberal global economic order. Notably, China has shown little interest in addressing the two global imbalances that it has caused with its own large external surplus and excess of domestic savings over investment.

Meanwhile, smaller countries and middle powers have mostly played the quiet game, pursuing independent bargains with Trump and hoping to limit the damage to their own economies. The exception is Brazil, whose president, Luiz Inácio Lula Da Silva, has emerged as the rare exemplary leader who refuses to grovel at Trump’s feet. Despite facing punitive 50% tariffs and pointed personal attacks, he has proudly defended his country’s sovereignty, democracy, and independent judiciary. As the New York Times puts it, “There is perhaps no world leader defying President Trump as strongly as Mr. Lula.”

Such leadership has been sorely lacking around the world. In India, the political commentator Pratap Bhanu Mehta points out that many business and political elites are searching for ways to accommodate Trump. But in doing so, Mehta argues, they are misreading him and the world he is creating. At any other time in recent history, the Trump administration’s behavior would immediately be called out for what it is: imperialism – plain and simple.

Imperialism must always be challenged – not accommodated – and that requires both power and purpose. Of course, America has held the reins of the world economy for a very long time. The dollar is firmly entrenched, and the US market remains singularly important. But these advantages are not as strong as they used to be. It would defy political logic and the laws of economic gravity if a country controlling only 15% of the world economy (in terms of purchasing power parity) could dictate the rules of the game to everyone else. Though the rest of the world remains divided, surely everyone has a common interest in repelling Trumpian imperialism – and thus in uniting to resist his demands.

Finding common purpose is perhaps the bigger challenge. If Trump “wins,” it will be because other large economies were unable (or unwilling) to articulate an alternative framework for the global economy. Pining after traditional multilateralism and global cooperation – as many targets of Trump’s ire have done – is of little use and merely signals weakness.

The world needs new ideas and principles for avoiding both the instabilities and inequities of hyper-globalization and the destructive effects of beggar-thy-neighbor policies. It is not realistic to expect a new Bretton Woods agreement. Nevertheless, middle powers and large economies can still model such principles by putting them to work in their own policies.

Trump’s actions have held up a mirror to others, and most should recognize that their reflection is not a pretty sight. Fortunately, their apparent helplessness has been self-imposed. It is not too late to choose self-confidence over humiliation.

Dani Rodrik, Professor of International Political Economy at Harvard Kennedy School, is Past President of the International Economic Association and the author of the forthcoming Shared Prosperity in a Fractured World: A New Economics for the Middle Class, the Global Poor, and Our Climate (Princeton University Press, November 4, 2025).

Aug 8, 2025

DANI RODRIK

US President Donald Trump’s reckless, self-destructive tariffs have given Europe, China, and various middle powers an opportunity to make a statement about who they are and what they stand for. With few exceptions, their responses have left much to be desired.

CAMBRIDGE – America’s critics have always depicted it as a selfish country that throws its weight around with little regard for others’ well-being. But President Donald Trump’s trade policies have been so misguided, erratic, and self-defeating as to make even the most cartoonish of such descriptions seem flattering. Still, in a twisted way, his trade follies have laid bare other countries’ failures as well, by forcing them to consider what their responses say about their own intentions and capabilities.

It is said that one’s true character is revealed in the face of adversity, and the same goes for countries and their political systems. Trump’s frontal assault on the world economy was a shock to everyone, but it also gave Europe, China, and various middle powers an opportunity to make a statement about who they are and what they stand for. It was an invitation to articulate a vision of a new world order that could overcome the imbalances, inequities, and unsustainability of the old one, and that would not depend on the leadership – for better or worse – of a single powerful country. But few rose to the challenge.

In this respect, the European Union has perhaps been the greatest disappointment. In terms of purchasing power, it is almost as large as the United States – accounting for 14.1% of the world economy, compared to 14.8% for the US and 19.7% for China. Moreover, despite the recent rise of the far right, most European countries have avoided backsliding into authoritarianism. As a collection of democratic nation-states whose geopolitical ambitions do not threaten others, Europe has both the power and the moral authority to provide global leadership. Instead, it dithered and then submitted to Trump’s demands.

Europe’s ambitions were always narrowly parochial; but in folding to Trump, it is not even clear that it served its own immediate interests. The July handshake deal between Trump and European Commission President Ursula von der Leyen leaves 50% tariffs on European exports of steel and aluminum, places 15% tariffs on most other exports, and commits Europe to ridiculously high levels of energy imports from the US. Rarely has the EU’s structural weakness as a confederation of countries without a collective sense of identity been on starker display.

China has played a tougher game, retaliating forcefully with its own tariffs and restricting exports of critical minerals to the US. Trump’s vindictive, self-defeating foreign policies have helped China extend its influence and enhance its credibility as a reliable partner for the developing world. But the Chinese leadership has also failed to articulate a practical model for a post-neoliberal global economic order. Notably, China has shown little interest in addressing the two global imbalances that it has caused with its own large external surplus and excess of domestic savings over investment.

Meanwhile, smaller countries and middle powers have mostly played the quiet game, pursuing independent bargains with Trump and hoping to limit the damage to their own economies. The exception is Brazil, whose president, Luiz Inácio Lula Da Silva, has emerged as the rare exemplary leader who refuses to grovel at Trump’s feet. Despite facing punitive 50% tariffs and pointed personal attacks, he has proudly defended his country’s sovereignty, democracy, and independent judiciary. As the New York Times puts it, “There is perhaps no world leader defying President Trump as strongly as Mr. Lula.”

Such leadership has been sorely lacking around the world. In India, the political commentator Pratap Bhanu Mehta points out that many business and political elites are searching for ways to accommodate Trump. But in doing so, Mehta argues, they are misreading him and the world he is creating. At any other time in recent history, the Trump administration’s behavior would immediately be called out for what it is: imperialism – plain and simple.

Imperialism must always be challenged – not accommodated – and that requires both power and purpose. Of course, America has held the reins of the world economy for a very long time. The dollar is firmly entrenched, and the US market remains singularly important. But these advantages are not as strong as they used to be. It would defy political logic and the laws of economic gravity if a country controlling only 15% of the world economy (in terms of purchasing power parity) could dictate the rules of the game to everyone else. Though the rest of the world remains divided, surely everyone has a common interest in repelling Trumpian imperialism – and thus in uniting to resist his demands.

Finding common purpose is perhaps the bigger challenge. If Trump “wins,” it will be because other large economies were unable (or unwilling) to articulate an alternative framework for the global economy. Pining after traditional multilateralism and global cooperation – as many targets of Trump’s ire have done – is of little use and merely signals weakness.

The world needs new ideas and principles for avoiding both the instabilities and inequities of hyper-globalization and the destructive effects of beggar-thy-neighbor policies. It is not realistic to expect a new Bretton Woods agreement. Nevertheless, middle powers and large economies can still model such principles by putting them to work in their own policies.

Trump’s actions have held up a mirror to others, and most should recognize that their reflection is not a pretty sight. Fortunately, their apparent helplessness has been self-imposed. It is not too late to choose self-confidence over humiliation.

Dani Rodrik, Professor of International Political Economy at Harvard Kennedy School, is Past President of the International Economic Association and the author of the forthcoming Shared Prosperity in a Fractured World: A New Economics for the Middle Class, the Global Poor, and Our Climate (Princeton University Press, November 4, 2025).

Monday, August 25, 2025

Jerome Powell’s Good News on Interest Rates Is Not Necessarily Good News

Dean Baker, via Patreon

The stock market rallied big-time on Friday as Federal Reserve Board Chair Jerome Powell indicated that the Fed was likely to lower interest rates at its September meeting. In assessing whether a rate cut is appropriate, Powell was looking at the higher inflation caused by the Trump tariffs and trading it off against the signals of a weakening labor market from the monthly jobs reports and other data.

The key issue is, as posed by Powell:

“The question that matters for monetary policy is whether these price increases are likely to materially raise the risk of an ongoing inflation problem. A reasonable base case is that the effects will be relatively short lived—a one-time shift in the price level. Of course, "one-time" does not mean "all at once." It will continue to take time for tariff increases to work their way through supply chains and distribution networks. Moreover, tariff rates continue to evolve, potentially prolonging the adjustment process.

“It is also possible, however, that the upward pressure on prices from tariffs could spur a more lasting inflation dynamic, and that is a risk to be assessed and managed. One possibility is that workers, who see their real incomes decline because of higher prices, demand and get higher wages from employers, setting off adverse wage–price dynamics. Given that the labor market is not particularly tight and faces increasing downside risks, that outcome does not seem likely.”

To summarize, there is no doubt that the economy is seeing higher inflation as a result of the tariffs. Powell is asking whether this is likely to be a one-time uptick in the inflation rate, which then settles back down (transitory), as long as tariffs are not raised further; or, if the uptick in inflation could spark more rapid wage growth as workers try to protect their real wage.

The “encouraging” assessment from Powell is that the signs of weakness in the labor market mean this is not likely. That means that workers will effectively have to eat the tariffs in the form of lower real wages.

That is good news from the standpoint of keeping inflation down, but it is bad news from the standpoint of workers trying to pay their bills. Powell is saying that he does not believe the labor market is currently strong enough for them to secure pay increases to cover the costs imposed by Trump’s tariffs.

I am inclined to agree with Powell on this point, the labor market does look like it is weakening. Workers are reluctant to quit their jobs and hiring has slowed. Also, it appears the rate of wage growth has slowed moderately from around 4.0 percent in 2023 and 2024, to a 3.7 percent rate in the last three months compared with the prior three months.

The slowing for the lowest paid workers in hotels and restaurants seems to be even sharper, with the rate being just 2.5 percent. So, Powell is probably right that workers will likely have to eat the bulk of the inflation caused by Trump’s tariffs.

Unfortunately, a rate cut by Powell may not do as much to boost the economy as many hope. The short-term rate set by the Fed has little direct effect on the economy. Most of the impact of lower rates is from a reduction in longer-term rates, and especially the 30-year rate that matters for mortgages.

In the last year, the gap between the interest rate on 30-year bonds and 10-year bonds has grown considerably. At the end of August last year, the interest rate on 30-year bonds was roughly 4.15 percent, 30 basis points higher than the 3.85 percent rate on 10-year bonds. Currently it is almost 4.9 percent, 60 basis points higher than the 4.26 percent rate on Treasury bonds last Friday.

It is likely that concerns about higher inflation and/or Trump craziness is responsible for the growth in this gap. If this gap grows further, it raises the possibility that lower interest rates from the Fed will have a limited impact on the housing market and the economy.

This is where Trump’s bullying of the Fed has a perverse impact. Chair Powell has insisted that the Fed’s policy will be moved by the data, not hectoring from Trump, and I believe he has stuck to this position even if he does lower rates in September. FWIW, I don’t consider it at all inappropriate for the President and/or his economic advisers to publicly make their case on interest rates, but that case should be based on evidence, not intimidation. The Fed is not a church.

But when Trump threatens to fire Powell, or now Governor Lisa Cook, if they don’t lower rates, it undermines confidence in the United States as a safe place to invest money. The net effect could well be to raise the longer-term rates that matter most for the economy. But it is understandable that a 79-year-old man suffering from dementia wouldn’t understand this.

Sunday, August 24, 2025

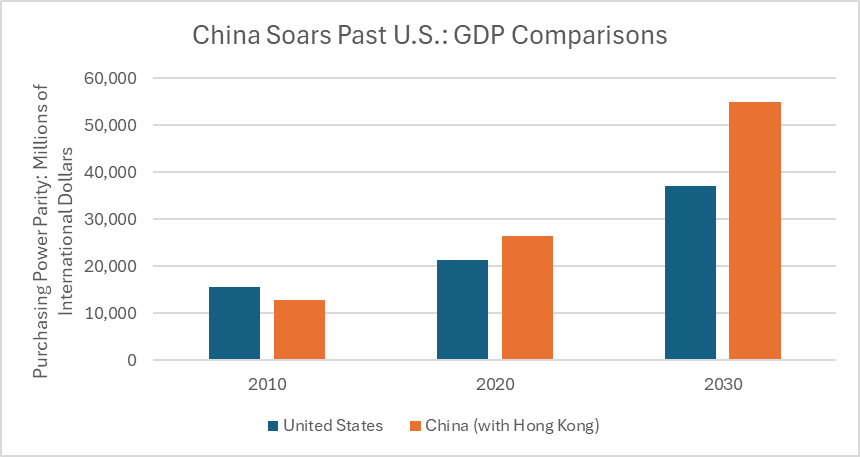

MAGA 2.0: Making China Great Again -- DEAN BAKER

In Donald Trump’s make-believe world prices are falling, the economy is booming, he is bringing peace all around the world, and gas costs less than $2.00 a gallon. But in the real-world inflation is increasing, the economy is stalling, wars are continuing, and gas costs more than $3.00 a gallon.

Ordinarily, we shouldn’t be bothered too much by the dreams of a 79-year-old man suffering from dementia, but we have little choice but to be bothered when that person is the president of the United States. Trump’s unreality is interfering with the reality for the rest of us in a very big way.

One way his hallucinations matter in a big way is his failure to come to grips with the fact that China is now the world’s dominant economy. By the end of this decade, the I.M.F. projects it to be nearly 50 percent larger than the U.S. economy.

Source: International Monetary Fund.

There is not much that the U.S. can do about this large and growing disparity. It can and should make sure that we have secure supply-chains for essential items, as the Biden administration tried to do. We also should take steps to promote economic growth here, not just to compete with China, but also to improve living standards for low and middle-income households. But we also need to come to grips with a world where the United States is still a very important actor, but no longer the world’s dominant economic power.

To my view, that would mean finding areas of cooperation with China for mutual benefit. The most obvious one would be sharing technology in health care and clean energy. It benefits both nations and the whole world if pandemics can be prevented or contained, diseases like cancer can be cured, and we manage to limit the damage from global warming.

Unfortunately, Trump seems determined to go 180 degrees in the opposite direction. His Secretary of Health and Human Services, RFK Jr., just threw a massive sledgehammer into the country’s biomedical research system by nixing mRNA research and haphazardly cancelling research grants in a variety of other areas.

The story on climate technology is even worse. Trump is actively trying to destroy the solar and wind industries, with a special animus towards the latter. He also is trying to block the transition to electric vehicles, taking away the credits put in place under the Biden administration. Meanwhile in China, electric vehicles already have more than half the market. Electric cars are cheap and recharging times are short.

With the world rapidly turning towards cheap and reliable clean energy, Trump has the United States doubling down on fossil fuels. This will have ramifications throughout the economy, most obviously in the power-hungry AI industry. China’s leading developers have the advantage of both being far more energy efficient and also having access to cheap and abundant electricity.

With all the ways Trump is acting to sabotage the U.S. economy, it seems far more likely U.S. GDP will be lower than the I.M.F’s projections for 2030 than higher. Beyond the attack on biomedical research, Trump is attacking university-based research more generally. His extortion efforts directed against pretty much all the major research institutions will impede progress everywhere. Many researchers have already moved to Europe, Canada, or elsewhere, where they don’t have to worry about a politician cutting off their funding in a temper tantrum.

Colleges and universities were also a major source of export earnings, as students from around the world saw getting a degree from a school here as an important credential in a wide variety of areas. That is not likely to continue to be the case when we have an administration that claims the right to deport them at any time for any reason. This will be a problem for foreign visitors more generally, whose travel contributed almost $220 billion (7.3 % of export earnings) to the U.S. economy in 2024.

Trump’s mass deportation will slow labor force growth to a trickle, as there will be few immigrants to offset the large-scale retirement of baby boomers. This slowing labor force growth was not factored into the I.M.F. projections.

Trump has also burned bridges with pretty much all of the United States’ traditional allies. While Europe, Canada, and the rest might humor Trump by accepting his trade deals, they are working as quickly as possible to diversify exports away from the U.S. market. On its current course, the United States will both have less economic leverage and virtually zero goodwill by 2030.

There is no inherent problem with a country other than the United States having the dominant world economy. After all, the rest of the world dealt with it for the last 100 years, and most countries did just fine. However, the United States would be much better positioned to deal with China as the pre-eminent economic power if we had leaders who lived in the real world. We don’t at present, and it is not clear at what point in the future this could change.

Sunday, August 10, 2025

Mike Roberts on WAPE

Michael Roberts Blogblogging from a marxist economist

WAPE 2025: geopolitics, economic models and multi-polarity

Last weekend the 18th Congress of the World Association of Political Economy (WAPE) took place in Istanbul, Turkey.. WAPE is a Chinese-run academic economics organisation, linking up with Marxist economists globally. “Even though that might seem like bias, the WAPE forums and journals still provide an important outlet to discuss all the developments in the world capitalist economy from a Marxist perspective. Marxist economists from all over the world are welcome to join WAPE and attend WAPE forums.” (WAPE mission statement).

As you would expect, many of the plenary speeches included economists from China as well as those from ‘the West’ and the ‘Global South’. I was invited to attend but was unable to do so, so I cannot report on the subjects of the various plenary speeches. However, I did make a presentation by recorded video (see my You Tube channel).

There were also a series of paper sessions covering themes such as geopolitical economy; macroeconomic modelling; ecology; AI; imperialism and multi-polarity; and of course, China. I have managed to obtain some of the presentations from their authors and so can make some (rather limited) comments.

Let’s start with geopolitics. The first paper session on this theme was about the 80th anniversary of the United Nations. I’m afraid I cannot comment on the papers in this session as I do not have them. But I can make a general point about the history and efficacy of the UN. It was an institution set up in 1945 along with other agencies designed to set the world order after WW2. The IMF was supposed to support advanced capitalist economies that got into financial trouble, using funds mainly financed by the US; the World Bank was supposed to support and help the poor countries of the world to grow and end their poverty; and the UN was supposed to be the international body to ensure peace and offer ‘neutral’ peace-keeping diplomacy and armed forces if necessary to resolve or control conflicts.

The claim was that these organisations were fair and balanced and constructive. In reality, they were agencies to ensure US-led imperialist control over the world. The IMF provides emergency funds under strict conditionalities; but many countries that have governments working in the interests of US imperialism get extra help with fewer conditions (Argentina, Ukraine) while others are starved of funds (Venezuela) or face distress from IMF debt. Based in New York, the UN was not a body of equals; it has a security council where only the top post-war nations have a vote and a veto on anything that the UN does. This has paralysed its role as peacekeeper. Significantly, as the US has lost some of its dominance politically, the UN it has increasingly been ignored by the great powers – whereas the US would go to the UN to get backing for its war in Korea in the 1950s or even the invasion of Iraq in the 2000s (unsuccessfully), increasingly the US now looks for ‘coalitions of the willing’ to bypass the UN and instead uses and expands NATO for its purposes. The UN has not played a role in resolving conflicts in Ukraine, Gaza, Iran or Afghanistan. It is an irrelevance.

That the UN is an irrelevance is further confirmed by the discussions taking place at WAPE and other conferences of the left. The discussion now is about alternatives to US hegemony and imperialism and the hope that ‘multipolarity’, as expressed in the BRICS formation, could be a new development in defeating US dominance over the last 80 years.

There were a number of papers on this theme. I have only one that I can comment on. Prof. Chandrasekhar Saratchand, University of Delhi presented: Neoliberalism and the Transition From the Washington Consensus to MAGA. In his paper, Prof Saratchand argues that the global order post WW2 as described above gave way to neoliberalism, the aim of which was to extract extra surplus value out of the Global South by ‘metropolitan capital’. The so-called Washington Consensus (WC) was the ideological support for this exploitation of the poor countries. The WC argued that only the US and the ‘free democracies ‘ of the West could bring prosperity through “free markets” and unrestricted capital flows. Any resistance to this Consensus by government adopting protectionism or nationalisation was detrimental to the world.

However, China’s rise increasingly undermined the world order (ie US hegemony). So the US switched from ‘engagement’ with China to ‘containment’. The Washington Consensus was also amended post the Great Recession to no longer advocate globalisation and free trade, but instead to support the ‘democratic bloc’ against the ‘autocratic bloc’. Saratchand argues that the US cannot turn the clock back and stay as global leader, despite the aims of the MAGA supporters under Trump in the US. Indeed, the dollar is threatened by multi-polar blocs in the future.

My own paper (as presented by video above) concentrated on the failure of the poor countries of the world to ‘catch up’ with the rich countries after 80 years of the post-war world order. I tried to gauge the gap between the rich and poor countries ie the imperialist core and the dominated periphery. To do this, I measured 1) the average per capita income in each country (taking into account, where we can, the inequality of incomes within countries); 2) the level of labour productivity; and 3) ‘human development’ as defined by the UN. Then I extrapolated the current average growth in these measures to see when the periphery might catch up.

I found that the countries of the Global South (6bn people) are not ‘catching up’ with the Global North (2bn people) and never will in the foreseeable future. The main reasons are that wealth (value) is being persistently transferred from the South to the North AND profitability in the Global South is falling faster than labour productivity growth is rising. However, I did find that China may be the exception because its investment growth is less determined by profitability than in any other major Global South economy. In effect, the Marxist model of uneven and combined development explains best why the periphery is not catching up and will not do so unless the structure of global accumulation and trade is changed – to put it bluntly, unless capitalism/imperialism is replaced by a commonly owned and democratically planned global economy.

Another theme of the conference sessions was macro modelling, in other words working out the cycles of accumulation and growth under capitalism. Costas Passas, a the Greek School of Social Sciences looked at Greek capitalism in his presentation, The Political Economy of Crisis and Recovery in Modern Greece. This was a joint paper with Thanasis Maniatis, both of whom published in our book World in Crisis back in 2018. Passas and Maniatis show that, contrary to recent optimistic mainstream talk, Greece is not really recovering from the terrible years of debt and austerity of the 2010. The central role in any model of capitalism must be profitability; and the current modest recovery in Greece is due to a huge increase in exploitation and an unprecedented devaluation and destruction of capital, the two forces that can raise profitability. But Greek capital still has a very low level of profitability, and so insufficient investment holds back technical change. All the old problems of a weak capitalist economy are exhibited in a renewal of balance of payments problems in Greece. For more on this, see my recent online booklet on Greece.

In another paper, Hiroshi Onishi and Chen Li, of Keio University–Kyoto University and St. Andrew’s University, considered what they called an External Dependency Model of the Capitalist Sector in Labour Supply. They construct an accumulation model based on two assumptions that (1) the level of wages determines the supply of labor; and (2) labor shortages are historically offset by the non-capitalist sector.

This seems to follow the idea of Rosa Luxemburg that capitalist progress depends on the extent of labour supply or demand, not on the relation between the productivity of labour and profitability. Onishi and Chen Li argue that the greater the labor supplied from outside—whether from foreign countries or from non-capitalist sectors such as rural areas—the more intensely capitalists have been able to exploit labor within the capitalist sector. As Western societies become increasingly unable to accept more immigrants due to rising cultural tensions, and as rural labor reserves in Asia become depleted, the exploitation rate will fall, causing a crisis for capitalism. This echoes the theory of the great economic historian J Arthur Lewis.

It is true that immigration and an increased supply of labour is a powerful counteracting factor to falling profitability in capitalist economies, ie it produces a rise in the absolute rate of surplus value. But the presenters seemed to have ignored the most important way capitalism accumulates and expands, ie through mechanisation and thus a rise in relative surplus value. The end of immigration does not necessarily mean a fall in exploitation and therefore a fall in profitability. Unfortunately, Rosa Luxemburg was wrong to think capitalism would collapse if external demand from the periphery fell, and neither is it correct to think capitalism would collapse if the supply of labour globally dried up, even though that would intensify the problem of boosting profitability for capital.

Konstantinos Loizos at the Centre of Planning and Economic Research (KEPE), and Stavros Mavroudeas at Panteon University, Athens, presented a paper Alternative Marxist Theories of Competition: Looking for a New Comprehensive Hypothesis. This argued that any Marxist theory of competition between capitals must involve class struggle as the key element. They refer to Marxist ‘fundamentalists’ (of which I think I am one) who “are right to point out the importance of competition to support innovation in capitalist development.” However, the defining characteristic of capitalism is not competition, but class struggle. The authors argue that class struggle takes two forms: among capitals and between capital and labor and both determine the rate of surplus value and the rate of profit.

Surely, it is the exploitation by capital of labour that determines the size of surplus value and profitability, while competition among capitals determines the distribution of that surplus. For me, the class struggle is between capital and labour. Competition among capitals is not a ‘class struggle’? Many capitals are not many classes. So for me, the charge that “fundamentalists seem to degrade a social relation with political consequences to a technical issue that justifies the tendency for equalization of the rates of profit” is an odd conclusion. If the authors mean that academic Marxists are only ‘interpreting’ the world when ‘the point is to change it’, then there may be truth in that, but to talk of Marx’s law of profitability as a ‘fatalistic law’ that degrades the role of class struggle cannot be right.

Perhaps the most interesting paper presented at WAPE that I have received is that by Greek Marxist economists Ozan Mutlu & Lefteris Tsoulfidis, on Capital Accumulation, Technological Change, and the Rate of Profit in European and the US Economies. This paper makes a significant contribution to Marx’s law of profitability and the ensuing consequences for the major economies in 2025.

In the paper, the authors break up the economies of Europe and the US into productive and unproductive labour sectors and generate rates of profit accordingly. The general rate of profit is for total economy and the net rate of profit is for productive sectors only. They confirm a long run downward trend in the profitability of capital, driven by two factors: a rising organic composition of capital and a rising share of surplus value going into unproductive activities. This leads to a fall in investment over time to “what can be termed “Marx’s moment” or the tipping point of “absolute overaccumulation of capital” as in 2008.

However, a recent development has been a reversal of a rising share of surplus value in the unproductive sectors, which “appears to have contributed to stabilizing the profit rate” since 2008. The authors speculate this reversal could be due to “new technologies (AI? – MR) increasingly being applied to non-production activities, where employment has sharply declined. This is evident in sectors such as finance, real estate and wholesale and retail trade. These trends seem likely to solidify soon and will probably shape the emerging new sixth-long cycle.” The authors refer here to their view that capitalism is in its downward phase of a fifth long cycle and a new sixth cycle may soon start, driven by rising profitability. I am not so sure. https://thenextrecession.wordpress.com/2025/07/27/ai-bubbling-up/

A final point. WAPE contributors are keen to discuss and analyse the possible decline of US hegemony and the rise of a ‘multipolar’ world, personified mainly in the BRICS group. It seems many on the left look to the BRICS to provide an alternative anti-imperialist force that can resist US imperialism in support of working people globally.

I think this is a dangerous illusion. Can we really expect that Putin’s Russia, Xi’s China, Modi’s India, Ayotolla’s Iran, El-Sisi’s Egypt, Subianto’s Indonesia or MbS in Saudi Arabia will lead an internationalist movement of workers to overthrow imperialism? These governments do not work for the international interests of working people, but for the national interests of their respective elites. The ‘class struggle’ globally is between the workers of all these countries and their ruling elites, not between elites of imperialism and the elites of the ‘resistant’ countries. For me, imperialism will only be defeated by movements of the working class in the rich countries, but also in the BRICS.

Apologies to anybody with papers not reported on, or for any misunderstanding of the arguments of those I did consider.

Tuesday, July 22, 2025

Intro to West Virginia Polical Economy: Summary

An Introduction to West Virginia Political Economy

The charts and remarks below consitute an exploration into West Virginia public and private material, service and farm production, employment, workforce, compensation, surpluses, taxation and subsidies, population. These are the categories of the state's political economy, since it embraces the various public and private components that are used to structure and measure overall economic performance . These are also the categories, by industry, that the BEA uses to inform policy advice of legislators and other federal departmetns, as well as the banking and financial services consumers.

The data available from BEA (Bureau of Economic Analysis), ranges from 2017-2022.

GDP

West Virginia GDP -- What and how much do we produce?

The underlying story in this graph is twofold:

- a) the heavy concentration of West Virginia's gross product value in natural resources and energy -- two markets that were heavily impacted by the pandemic and associated supply-chain failures, as well as the sanctions against Russian oil in the wake of the Ukraine war, as well as overall impact of monopoly in passing on price increases in global markets to consumers.

- b) Overall real growth is very SLOW.

Real GDP by Industry

The values in this chart are billions of dollars. Both 'B' and 'G' in the graph notation stand for 'billion'. This graph focuses on the most recent available regional industrial data, 2022. This permits displaying the distribution of production values across industries, and, by inference, occupations. The latter calculation integrates data from both BEA (commerce dept) and BLS (Bureau of Labor Statistics) to arrive at the sector employment estimates. The values are in millions.Note: for purposes of calculating GDP, health care services generated nearly as much dollar value as mining. BUT, it turns out health care is also significantly subsidized and thus, not really taxable.

GDP per employee

(This is a rough calculation of worker productivity, even though

it does not distinguish between full and part-time work)

Employment by Industry

Compare Operational Surplus to Compensation by Industry

Subscribe to:

Posts (Atom)

-

John Case has sent you a link to a blog: Blog: Eastern Panhandle Independent Community (EPIC) Radio Post: Are You Crazy? Reall...

-

The Intersectionality that Dare Not Speak Its Name Peter Dorman http://econospeak.blogspot.com/2017/03/the-intersectionality-that-dare-not.h...

-

via Bloomberg -- excerpted from "Balance of Power" email from David Westin. Welcome to Balance of Power, bringing you the late...

via Bloomberg -- excerpted from "Balance of Power" email from David Westin. Welcome to Balance of Power, bringing you the late...