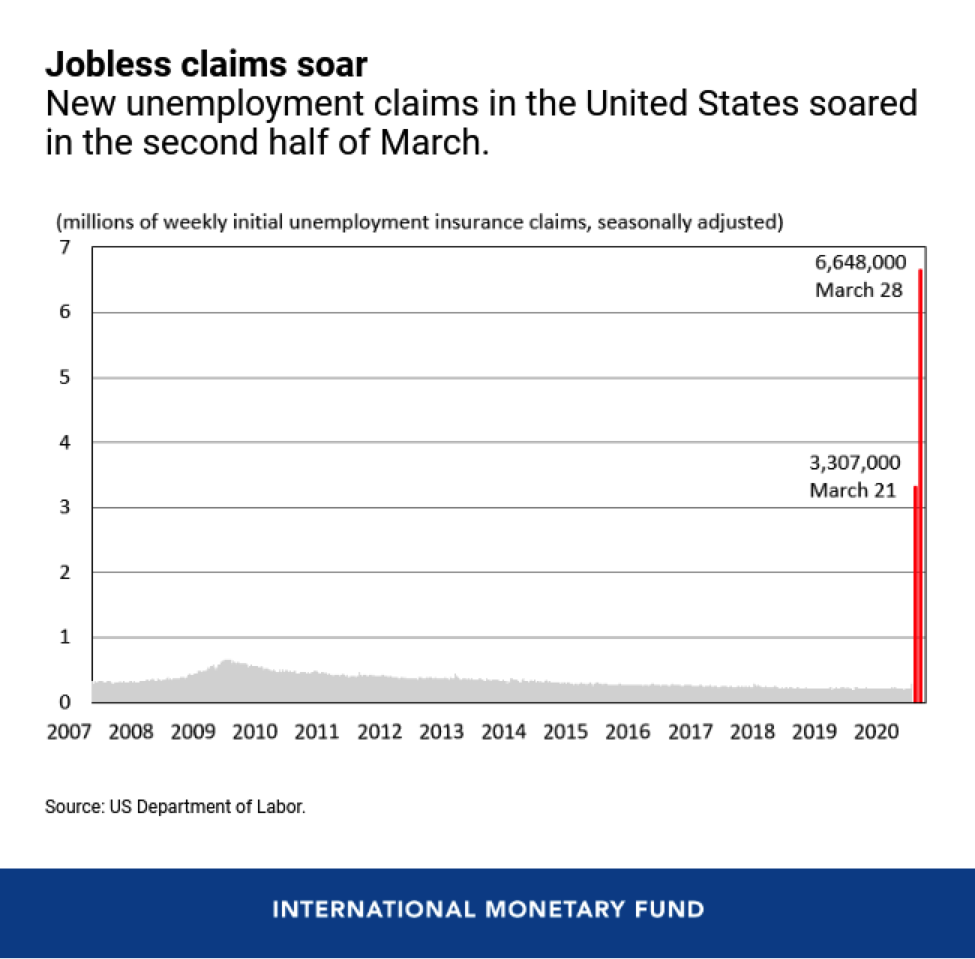

Payrolls fell by 701,000 in March, their first monthly decline in almost 10 years, and the jobless rate ticked up to 4.4 percent (from 3.5) as the coronavirus and efforts to contain it pounded the U.S. labor market last month. Because of the timing in the surveys in this report, it only picks up the front end of tsunami of layoffs that occurred in the second half of March, when initial claims for Unemployment Insurance rose by almost 10 million, an increase most economists would have considered inconceivable before this crisis. But the report clearly identifies the tip of the wave.

The surveys were fielded in the middle of March, and thus better reflect conditions in the first half of the month, when containment measures were just taking hold. Commerce, travel, and broad consumer activity was slowing but hadn't shut down as they would in March's second half. Even so, the report is far more negative than recent vintages, and shows how remarkably quickly conditions have reversed in the job market.

For example, the 0.9 point increase in the jobless rate was the largest one-month increase since 1975; the 1.7 point increase in the underemployment rate, to 8.7 percent, is the largest increase on record since this measure was introduced in 1994. The Bureau reports that the "bulk of the increase in unemployment occurred among people on temporary layoff, which increased 1.0 million in March to 1.8 million." Measures of labor market participation also fell sharply, a clear reflection of the reversal in labor demand. This shift is especially disheartening as prior to the virus, the tight job market was pulling typically left-behind workers into the job market. Such gains are quickly unraveling, a point I return to below.

As readers know, we typically feature our jobs smoother which averages monthly payroll changes over 3, 6, and 12 month windows in order to pull out the underlying signal. We print the smoother below, but it too is less informative this month, since a backwards looking average by definition downplays the sharp shift in trend that occurred in the past two weeks (to emphasize this point, we include a bar for the 701K loss in March alone).

A better, simpler approach this month is to plot monthly payroll levels, which show the sharp trend reversal in March.

Hourly pay stayed on track last month, up 3.1 percent and beating inflation that's been running just north of 2 percent, though price growth will likely slow (boosting real wage growth) due to very low energy prices. However, wage trends can be deceptive at times like this because of "composition effects." For example, as more low-wage workers face layoffs relative to high-wage workers, this can show up as accelerating wage growth. I'll try to parse out this potential bias in forthcoming reports.

Different sectors have different degrees of exposure to the jobs impact of the virus, of course. One way to think of this difference is that if you can draw a paycheck by clicking into Zoom meetings, you're in a less exposed sector. So, restaurant, hotel workers, flight attendants and anyone in a face-to-face services (and their suppliers) has a much higher chance of a layoff relative to many in professional services like legal, accounting, or research. The food vendor who works at a professional sports venue is directly exposed; the team's lawyer is not.

For example, employment in restaurants and bars fell by over 400,000 in March, a one-month loss of over 3 percent, by far the sector's worse month on record. Conversely, employment in professional and technical services was up slightly in March, by about 6,000. True, that's a weak month for the sector, and most sectors (outside of those that are directly responsive to containment efforts) are being hit by the sharp downturn. But magnitudes of losses will differ by exposure.

It is far from incidental, of course, that there's an inequality divide implicit in that distinction. A useful analysis from the St. Louis Federal Reserve split workers by occupations into high and lower risk of unemployment. About half of the workforce fell into each category (to be clear, that doesn't mean unemployment will hit 50 percent; not every exposed worker will get laid off). The analysis found that "the highest risk of unemployment also tend to be lower-paid occupations. The average annual earnings of the low-risk occupations is $64,600, about 75% higher than earnings in the high-risk occupations, at $36,600. This indicates the economic burden from this health crisis will most directly affect those workers who are likely in the most vulnerable financial situation."

Source: Charles Gascon, St. Louis Fed.

We've never shut the U.S. economy down as we have done in response to the virus. This was a wholly necessary response to its threat, but it came at point when the labor market was persistently closing in on full employment, providing meaningful employment and wage gains for workers who are often left behind under more slack conditions. Much as full employment provides out-sized benefits for the most vulnerable workers, the reversal we're now witnessing metes out the most pain on those same groups of workers. Many of these laid off workers lack paid leave and their savings rate is zero or negative. That is, they are the least insulated among us against this sort of sudden shock.

That is why our relief efforts must scale to the unprecedented size of the problem. Recent stimulus measures, with their emphasis on checks to household and expanded Unemployment Insurance, are a good start but we a) must ensure these measures are quickly implemented, and b) we will need further trips back to this well.

The risk at times like these–risks we've seen borne out in both the health and economic responses–is doing too little. As Dr. Fauci said the other day (paraphrasing): If you think I'm overreacting, I'm probably getting it right.

-- via my feedly newsfeed

CAMBRIDGE – Crises come in two variants: those for which we could not have prepared, because no one had anticipated them, and those for which we should have been prepared, because they were in fact expected. COVID-19 is in the latter category, no matter what US President Donald Trump says to avoid responsibility for the unfolding catastrophe. Even though the coronavirus itself is new and the timing of the current outbreak could not have been predicted, it was well recognized by experts that a pandemic of this type was likely.

Add to Bookmarks

PreviousNext

SARS, MERS, H1N1, Ebola, and other outbreaks had provided ample warning. Fifteen years ago, the World Health Organization revised and upgraded the global framework for responding to outbreaks, trying to fix perceived shortcomings in the global response experienced during the SARS outbreak in 2003.

In 2016, the World Bank launched a Pandemic Emergency Financing Facility to provide assistance to low-income countries in the face of cross-border health crises. Most glaringly, just a few months before COVID-19 emerged in Wuhan, China, a US government report cautioned the Trump administration about the likelihood of a flu pandemic on the scale of the influenza epidemic a hundred years ago, which killed an estimated 50 million people worldwide.

Just like climate change, COVID-19 was a crisis waiting to happen. The response in the United States has been particularly disastrous. Trump downplayed the severity of the crisis for weeks. By the time infections and hospitalizations began to soar, the country found itself severely short of test kits, masks, ventilators, and other medical supplies.

The US did not request test kits made available by the WHO, and failed to produce reliable tests early on. Trump declined to use his authority to requisition medical supplies from private producers, forcing hospitals and state authorities to scramble and compete against one another to secure supplies.

Delays in testing and lockdowns have been costly in Europe as well, with Italy, Spain, France, and the United Kingdom paying a high price. Some countries in East Asia have responded a lot better. South Korea, Singapore, and Hong Kong appear to have controlled the spread of the disease through a combination of testing, tracing, and strict quarantine policies.

Interesting contrasts have emerged within countries as well. In northern Italy, Veneto has done much better than nearby Lombardy, largely owing to more comprehensive testing and earlier imposition of travel restrictions. In the US, the neighboring states of Kentucky and Tennessee reported their first cases of COVID-19 within a day of each other. By the end of March, Kentucky had only a quarter of the number of cases as Tennessee, because the state acted much more quickly to declare a state of emergency and close down public accommodations.

For the most part, though, the crisis has played out in ways that could have been anticipated from the prevailing nature of governance in different countries. Trump's incompetent, bumbling, self-aggrandizing approach to managing the crisis could not have been a surprise, as lethal as it has been. Likewise, Brazil's equally vain and mercurial president, Jair Bolsonaro, has, true to form, continued to downplay the risks.

On the other hand, it should come as no surprise that governments have responded faster and more effectively where they still command significant public trust, such as in South Korea, Singapore, and Taiwan.

China's response was typically Chinese: suppression of information about the prevalence of the virus, a high degree of social control, and a massive mobilization of resources once the threat became clear. Turkmenistan has banned the word "coronavirus," as well as the use of masks in public. Hungary's Viktor Orbán has capitalized on the crisis by tightening his grip on power, by disbanding parliament after giving himself emergency powers without time limit.

The crisis seems to have thrown the dominant characteristics of each country's politics into sharper relief. Countries have in effect become exaggerated versions of themselves. This suggests that the crisis may turn out to be less of a watershed in global politics and economics than many have argued. Rather than putting the world on a significantly different trajectory, it is likely to intensify and entrench already-existing trends.

Momentous events such as the current crisis engender their own "confirmation bias": we are likely to see in the COVID-19 debacle an affirmation of our own worldview. And we may perceive incipient signs of a future economic and political order we have long wished for.

So, those who want more government and public goods will have plenty of reason to think the crisis justifies their belief. And those who are skeptical of government and decry its incompetence will also find their prior views confirmed. Those who want more global governance will make the case that a stronger international public-regime health could have reduced the costs of the pandemic. And those who seek stronger nation-states will point to the many ways in which the WHO seem to have mismanaged its response (for example, by taking China's official claims at face value, opposing travel bans, and arguing against masks).

In short, COVID-19 may well not alter – much less reverse – tendencies evident before the crisis. Neoliberalism will continue its slow death. Populist autocrats will become even more authoritarian. Hyper-globalization will remain on the defensive as nation-states reclaim policy space. China and the US will continue on their collision course. And the battle within nation-states among oligarchs, authoritarian populists, and liberal internationalists will intensify, while the left struggles to devise a program that appeals to a majority of voters.