Wednesday, August 31, 2016

Eastern Panhandle Independent Community (EPIC) Radio: Big Day On Labor Beat Thursday on EPIC Radio

Eastern Panhandle Independent Community (EPIC) Radio: Big Day On Labor Beat Thursday on EPIC Radio: Big Day On Labor Beat Thursday on EPIC Radio Our new Call-In Line: 1-304-885-0708 OR -- if you are on Skype, just dial up jcase4218...

From newyorker.com: Obama Pays Mexico Five Billion Dollars to Keep Donald Trump

Obama Pays Mexico Five Billion Dollars to Keep Donald Trump

http://www.newyorker.com/humor/borowitz-report/obama-pays-mexico-five-billion-dollars-to-keep-donald-trump

Tuesday, August 30, 2016

Many Similarities, but Some Differences Between Cole, Justice [feedly]

Many Similarities, but Some Differences Between Cole, Justice

http://www.wvpolicy.org/many-similarities-but-some-differences-between-cole-justice/

-- via my feedly newsfeed

http://www.wvpolicy.org/many-similarities-but-some-differences-between-cole-justice/

Charleston Gazette-Mail – Both promise to bring back vanishing coal jobs, despite scant evidence that it's possible. Read

Both would fight West Virginia's drug epidemic by cracking down on dealers and pushing for increased treatment options for addicts.

Both want a pay raise for teachers but are vague on where the money would come from.

Neither supports Hillary Clinton for president.

There are quite a few similarities — more so than in most elections — between the two major party candidates for governor of West Virginia, Republican state Senate President Bill Cole and Democratic businessman Jim Justice.

-- via my feedly newsfeed

Bernstein: Context alert: Only 6% of those with health coverage get it through the “individual” market. [feedly]

Context alert: Only 6% of those with health coverage get it through the "individual" market.

http://jaredbernsteinblog.com/context-alert-only-6-of-those-with-health-coverage-get-it-through-the-individual-market/

-- via my feedly newsfeed

http://jaredbernsteinblog.com/context-alert-only-6-of-those-with-health-coverage-get-it-through-the-individual-market/

Every morning these days I'm greeted by front-page articles explaining how Obamacare is seriously broken as private insurers are abandoning the exchanges. No question, that's an important problem for the individual, or "non-group" market, though one with many good solutions (I'll provide links in a moment).

But anyone who makes this point should also be required to make this other point: only 6 percent of health care coverage is provided through the non-group market. About half of those with coverage get it through their employers, another third through public sources, leaving about 10 percent without coverage, down from 13 percent a few years ago (see figure below from the Kaiser Family Foundation; these data are for 2014; the uninsured rate fell another point in 2015).

Source: Kaiser Family Foundation

Neither the Post nor the Journal made this point, and my concern is that its omission leads too many readers to assume that the thinning of providers in the individual market is a fatal flaw as opposed to a manageable problem amenable to fixes.

To be very clear, a 6 percent problem is still a problem, and Obamacare has led to an increase in that corner of the market. But absent the correct context re its minority share, these articles provide the health law's opponents opportunities for over-heated rhetoric, claiming, for example, that we're seeing "the latest piece of evidence that Obamacare is a failed law built on false promises."

In fact, as the coverage trend suggests, Obamacare is working (a point the WaPo, to give credit where it's due, explicitly makes, citing both the coverage gains and various places with healthy competition in the exchanges). Yes, we need to recalibrate the rules around the non-group market. Good ideas to do so include:

–President Obama's idea to add a public option: "Congress should revisit a public plan to compete alongside private insurers in areas of the country where competition is limited. Adding a public plan in such areas would strengthen the Marketplace approach, giving consumers more affordable options while also creating savings for the federal government."

–Henry Aaron's idea to "Make the Obamacare exchange one big marketplace for everyone buying individual health insurance coverage. Nationwide, this would merge the 12 million people who get their insurance through Obamacare with the roughly 9 million who buy their policies outside the exchanges." To be clear, you'd have to do this state-by-state, requiring that any plan sold in that state's non-group market had to be sold through the exchange, so this is obviously a heavy lift in practice (so far, only DC and Vermont take this approach).

But Aaron's idea gets at the heart of the problem, which is expanding the "risk pool" within the individual market to avoid adverse selection problems that have been costly to private insurers, who priced too many of their products for a healthier pool than the one that showed up. My colleague Sarah Lueck offers good ideas on how to make needed risk-pool adjustments.

All that said, my key point here is one of perspective. Without context, a 6 percent problem gets inflated to be far more consequential for the ultimate success of Obamacare than it really is.

-- via my feedly newsfeed

Alan Kreuger: Human Capital in the 21st Century

Human

Capital

in the

21st

Century

I think it is fair to say that no French writer save Alexis de Tocqueville has been more influential in the United States than Thomas Piketty, director of studies at the elite Écoles des Hautes Études en Sciences Sociales in Paris and, most important here, author of Capital in the Twenty-First Century (Harvard University Press). Piketty's magnum opus has succeeded in achieving its goal of provoking a serious public discussion about a shadow hanging over capitalism, the rise in economic inequality.

The 700-page tome soared to the top of The New York Times' bestseller list, was praised by leading lights in the economics profession, venerated by op-ed columnists and assorted talking heads, and critiqued by serious social scientists and political partisans alike. Even if Capital… holds the record for the fewest pages read by the most purchasers (beating out Stephen Hawking's A Brief History of Time), it has provided an immense service by engaging the public in the economic theory of income distribution and by stimulating a sometimes-thoughtful discussion of the future course of inequality.

By this time, the book's strengths are widely known. It assembles and reviews centuries of data on capital's share of income in several countries. It gathers evidence on both the rate of return to capital and economic growth. It provides a provocative and intuitive theoretical argument predicting that income will become increasingly concentrated in the hands of capital owners and their heirs in the future if, as has been the case throughout much of history, the return on capital exceeds the growth rate of the economy. And it provides a sweeping perspective on economic history and the history of economic thought. Larry Summers, the former Treasury Secretary and president-emeritus of Harvard – and not one to suffer fools – called the book "a Nobel Prize–worthy contribution."

The U.S. may be headed for an inequality trap, where rising inequality in one generation reduces opportunities for economic advancement for disadvantaged children in the next generation, and so on into the future.

On the Other Hand…

Scholars have also raised some serious shortcomings with the analysis. No, I don't refer to the Financial Times' Chris Giles's overwrought and insignificant allegations of data errors (What is the world coming to when journalists can levy allegations at serious research without vetting, and yet command instant global attention?). Far more important issues have been raised by Per Krusell of Stockholm University and Tony Smith of Yale, for example, as to whether it is appropriate to assume (as Piketty does in what he calls the "second fundamental rule of capitalism") that capital's share of national income will tend toward the ratio of the savings rate to the growth rate in the long run.

The two economists note that the "fundamental rule" is untenable at one extreme (if growth falls to zero, savings would consume all of GDP) and that it is inconsistent with U.S. experience. They also point to alternative models of economic growth that are more consistent with U.S. experience. Serious related questions have been raised by Summers and others as to whether Piketty is sufficiently sensitive to the role of capital depreciation. Still others have pointed to the reality that inherited wealth is spread over multiple heirs, that heirs do not always invest wisely, and that many wealthy individuals choose to donate the bulk of their wealth to charitable causes rather than leave it to their offspring (thank you, Bill Gates and Warren Buffett).

I would yet raise another concern about Capital…, one that suggests that the evolution of inequality might be even more alarming than Piketty predicts. The focus of the book is on physical capital and financial capital. Human capital is given short shrift. Yet the importance of human capital – the investments that people make in their own productive capacities, just as capitalists invest in plant and equipment – is quite old in economics. In The Wealth of Nations, for example, Adam Smith wrote:

A man educated at the expence of much labour and time to any of those employments which require extraordinary dexterity and skill, may be compared to one of those expensive machines. The work which he learns to perform, it must be expected, over and above the usual wages of common labour, will replace to him the whole expence of his education, with at least the ordinary profits of an equally valuable capital.

In modern economies, the returns to human capital account for the lion's share of national income, and investment in human capital drives economic growth. (See, for example, my May 1999 paper in the American Economic Review: Papers and Proceedings for evidence on the outsized role played by human capital in the U.S. economy, and Paul Romer's 1990 Carnegie-Rochester Conference Series paper on human capital and growth.) Indeed, the categories referred to as labor's share of income and capital's share of income appear crude and antiquated when one can compare the share of income accruing to diverse groups ranging from managers to college graduates to high school dropouts.

A more troubling aspect of the Piketty phenomenon is not about what he might get wrong, but what he sweeps under the rug. While the increased concentration of income among the top 1 percent of Americans has attracted enormous attention in the wake of the American publication of Capital… and the earlier Occupy movement, the rise in income inequality among the bottom 99 percent is arguably a far more important feature of the economic landscape, and one at least as worrisome. Moreover, changes in earnings associated with different levels of education – that is, human capital – have played an outsized role in raising inequality among the bottom 99 percent of Americans.

Consider the following hypothetical calculation. If the top 1 percent's share of income had remained constant at its 1979 level, and all of the increase in share that actually went to the top 1 percent were redistributed to the bottom 99 percent – a feat that might or might not have been achievable without shrinking the total size of the pie – then each family in the bottom 99 percent would have gained about $7,000 in annual income (in today's dollars). That is not an insignificant sum. But contrast it with the magnitude of the income premium associated with educational achievement: The earnings gap between the median household headed by a college graduate and the median household headed by a high school graduate rose by $20,400 between 1979 and 2013 according to my calculations based on the Bureau of Labor Statistics' Current Population Survey. This shift – which took place entirely within the bottom 99 percent – is three times as great as the shift that has taken place from the bottom 99 percent to the top 1 percent in the same time frame.

The global wealth tax would not directly address rising inequality among the bottom 99 percent or do anything to provide more opportunities for those who are falling behind.

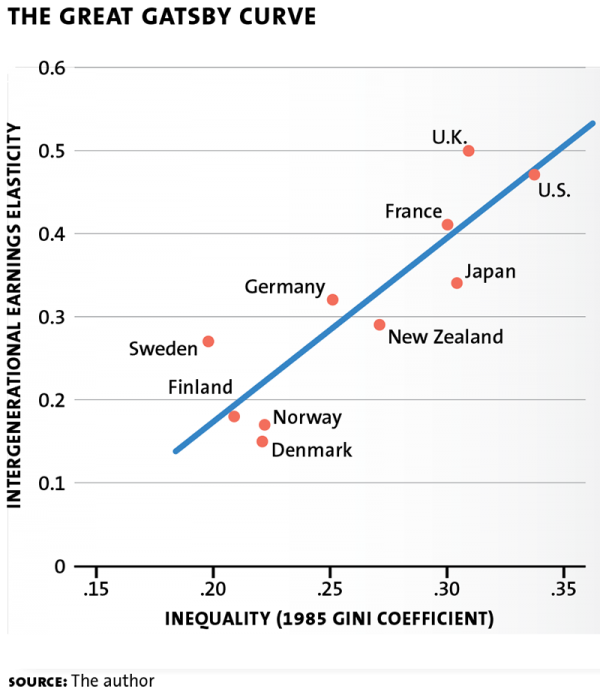

What's worse, there are reasons to believe that the enormous rise in inequality that we have experienced will reduce intergenerational economic mobility and cause inequality to rise further in the future. In 2012, I popularized a relationship that I called the Great Gatsby Curve (opposite page), based on earlier research by Miles Corak, Anders Björklund, Markus Jäntti and others. The Great Gatsby Curve shows that countries experiencing high inequality in one generation tend to have lower intergenerational mobility in the next. Raj Chetty and coauthors have shown that this relationship holds across labor markets within the United States as well and that higher inequality in the bottom half of the distribution is particularly predictive of lower intergenerational mobility.

The phenomenon of the Great Gatsby Curve is predicted by standard human capital theory. If the return to education increases over time, and higher-income parents are more prone to invest in the education of their children than lower-income parents – or if talents are inherited from one generation to the next – then the gap between children of higher- and lower-income families would be expected to grow with time. Furthermore, if social networking and family connections also have an important impact on outcomes in the job market, and those connections are transmitted across generations, one would expect the Great Gatsby effect to be even stronger.

There are, indeed, signs that the rise in income inequality in the United States since the late 1970s has been undermining equality of opportunity. For example, the gap in participation in extracurricular activities between children of advantaged and disadvantaged parents has grown since the 1980s, as has the gap in parental spending on educational enrichment activities. Furthermore, the gap in educational attainment between children born to high- and low-income parents has widened. The rising gap in opportunities between children of low- and high-income families does not bode well for the future.

Based on the rise in inequality that the United States has seen from 1985 to 2010 and the empirical evidence of a Great Gatsby Curve relationship, I calculated that intergenerational mobility will slow by about a quarter for the next generation of children. My concern – one entirely independent of Piketty's focus – is that the United States may be headed for an inequality trap, where rising inequality in one generation reduces opportunities for economic advancement for disadvantaged children in the next generation, and so on into the future.

What could prevent such an inequality trap from taking hold? The most obvious solution is to provide greater educational opportunities for children from less-privileged backgrounds. Universal preschool, for example, is a good place to start. It would also make sense to pay teachers in inner-city public schools who work with less-prepared and more-disruptive students substantially more than we pay those who work in fancy suburbs. By the same token, there's a good case to be made for funding smaller classes in poorer areas, especially in the early grades.

Consider, too, making better use of the summers for disadvantaged children. Much research establishes that kids from poor families fall further behind when school is out of session. Why not lengthen the school year, as Asia and Europe have done? Or provide vouchers that low-income families can use to enroll their children in educational activities in the summer?

These proposals contrast with Piketty's call for a global wealth tax to offset the forces driving rising inequality. Imposing and coordinating a wealth tax across nations is a political nonstarter. More important to my concerns, the tax would not directly address rising inequality among the bottom 99 percent or do anything to provide more opportunities for those who are falling behind.

Now, before I get carried away, I should also inject a word of caution. Capital… notes that deterministic predictions of rising or falling inequality – from Karl Marx to Nobel Prize–winner Simon Kuznets – have been wrong in the past. For example, the Kuznets Curve, which predicts that economic development will first increase income inequality and then decrease it, was long ago shown to be a relic of history by the careful research of Gary Fields of Cornell (which, curiously, is not cited by Piketty). As Fields wrote in 1999: "The Kuznets Curve is neither a law nor even a central tendency. The pattern is that there is no pattern." It is possible that the Great Gatsby Curve will go the way of the Kuznets Curve. Correlation, after all, is not causality.

To that point, it is possible that rapid developments in online education will greatly increase access to education and improve the quality of education. Moreover, the fact that inequality has increased at dramatically different rates in advanced countries over the past three decades suggests that country-specific institutions and policies have considerable ability to blunt or even prevent income inequality from rising. In this regard, one area where much evidence suggests that public policy can narrow the gap is worker bargaining power, such as by raising the minimum wage and tying it to the cost of living or by improving labor's leverage in collective bargaining.

But even if the Great Gatsby Curve does not hold over time, a large body of evidence suggests that the societal benefits of investing more in the education of children from disadvantaged backgrounds exceeds the costs. A global wealth tax, by contrast, is an untested idea without a chance of being adopted – and, if it were, would not adequately address the intergenerational mobility issue.

Piketty's Capital… may vanish from the public's consciousness as abruptly as it arrived. But generations of economists will continue to monitor income distribution for signs of whether his prediction of rising inequality, based on a seductively simple model of why income distribution changes, comes to pass. Piketty's forecast could well prove accurate for the wrong reasons, however – and, as a result, distract us from the core problem.

A vast body of research aimed at explaining rising inequality among the bottom 99 percent implicates the critical role of human capital – not to mention the significance of institutional changes including the fall in the real value of the minimum wage and the decline in union membership. If we lack the determination to address it in the context of the Great Gatsby Curve, the American Dream may turn into a distant memory.

John Case

Harpers Ferry, WV

Harpers Ferry, WV

The Winners and Losers Radio Show

7-9 AM Weekdays, Eastern Panhandle Independent Community (EPIC) Radio Stream,

Sign UP HERE to get the Weekly Program Notes.

Check out Socialist Economics.

Check out The EPIC Radio website

Did President Obama Threaten National Security in Negotiating the Trans-Pacific Partnership? [feedly]

This is a weak argument, full of assertions impossible for the ordinary citizen to verify....

http://cepr.net/publications/op-eds-columns/did-president-obama-threaten-national-security-in-negotiating-the-trans-pacific-partnership

The latest line from proponents of the Trans-Pacific Partnership (TPP) implies that President Obama threatened long-standing national security relationships in his negotiating of the TPP. These proponents are not pushing the economic merits of the TPP, but rather arguing that its rejection by Congress would jeopardize longstanding ties between the United States and Asia. The claim is that if Congress is not prepared to approve the TPP, then countries like Japan and South Korea will no longer be able to rely on defense commitments that have been in place for more than half a century.

As Singapore's Prime Minister Lee Hsien Loong, commented on a trip to Washington:

"It [rejecting the TPP] hurts your relationship with Japan, your security agreements with Japan, … And the Japanese, living in an uncertain world, depending on an American nuclear umbrella, will have to say: On trade, the Americans could not follow through; if it's life and death, whom do I have to depend upon?"

Other proponents of the TPP have made similar comments. The idea is that if the US won't follow through on a trade pact that is has spent almost eight years negotiating, then how can it be counted on to honor its defense commitments to the countries of the region.

If this claim is taken at face value, it implies that President Obama was unbelievably irresponsible in negotiating the TPP. He knew that many aspects of the deal would be highly controversial. For example, the deal includes no enforceable provisions to prevent the sort of currency management by China and other countries that have been the major cause of the country's $500 billion (2.8 percent of GDP) annual trade deficit.

The deal also includes provisions that make patent and copyright protection longer and stronger. These provisions will lead to higher prices for prescription drugs and other protected items in other countries, and possibly the United States as well. In addition, more money for the drug companies and entertainment industry in royalties means that our trading partners will have less money to spend on US manufactured goods.

In addition, the TPP provides for the creation of investor-state dispute settlement tribunals — extra-judicial bodies that give special privileges to foreign investors — including foreign subsidies of US corporations. These tribunals will be able to override US laws at all levels of government.

For these and other reasons, President Obama surely knew that the TPP would be highly controversial when it was debated before Congress. Is it really plausible that he did not make it clear to our negotiating partners that he couldn't guarantee approval of the final agreement?

The proponents of the TPP would have us believe that President Obama told our trading partners that approval of the TPP was a slam dunk. That they could count on congressional approval in the same way that they could count on Congress to honor its military commitments in the region. That one doesn't sound very likely.

In the lack of plausibility department we are also asked to believe that the governments in the region are incredibly ignorant about the state of US politics. The TPP has been a hot item for debate long before Congress voted to grant fast-track authority in the summer of 2015. It has continued to be a major issue in the presidential primaries of both parties. Is it plausible that the staffs of the Japanese, Vietnamese and other embassies of the TPP countries somehow missed these debates or failed to report back to their governments on how contentious the pact is?

That one hardly passes the laugh test. Surely these embassies are staffed by competent and intelligent people. It is precisely their job to follow debates like the one on the TPP and to report back to their governments. While the governments of the other countries in the TPP may be disappointed by the decision of Congress not to approve the pact, it is inconceivable that they would be surprised by it.

There is an alternative hypothesis that makes far more sense. The Obama administration, along with other supporters of the TPP, doesn't feel it can sell the deal based on its merits as an economic pact. Therefore they are inventing a national security rationale for the TPP that does not exist. It's not a pretty story, but as they say in Washington: You throw it against the wall and see what sticks.

-- via my feedly newsfeed

Robert Pollin on “Green Growth” [feedly]

Robert Pollin on "Green Growth"

http://triplecrisis.com/robert-pollin-on-green-growth/

-- via my feedly newsfeed

http://triplecrisis.com/robert-pollin-on-green-growth/

-- via my feedly newsfeed

Kuttner: Trumpism Could Be More Dangerous Than Trump [feedly]

Trumpism Could Be More Dangerous Than Trump

http://www.huffingtonpost.com/robert-kuttner/trumpism-could-be-more-da_b_11756020.html

-- via my feedly newsfeed

http://www.huffingtonpost.com/robert-kuttner/trumpism-could-be-more-da_b_11756020.html

Let's assume that the pundits and the polls are right. Hillary Clinton is on track to win the presidency. The Democrats may narrowly take back the Senate.

Can we exhale? No.

The fragility of American democracy and the pathology of our economy revealed by Trump (and by the appeal of Bernie Sanders) will still be with us. And it will take an extraordinary shift by President Hillary Clinton to move these deep tectonic plates.

In the short term, the forces of real hate have been loosed. They are not going away. Trump will have goons as poll watchers. He will find ways to insist that the election was stolen. He will continue to make more mischief, impeaching the legitimacy of our institutions.

After November, Trump may create a third party. He may create a media empire — or both. It is hard to imagine a pop culture political force more malign than, say, Limbaugh or Fox, but Trump will be it.

Medium term, all of the economic and cultural grievances brought to the surface by Trump and Sanders will still be there. Likewise the sluggish economy that doesn't create enough good jobs. Likewise the prospect of a lost economic generation. And the risk of more terrorist attacks.

All of this is soil for more Trumpism.

What defies conventional analysis is the clash of grievances. The groups that have played second fiddle to white men for so long are justifiably demanding a rightful place in our democracy and our economy. The multiple complaints of African-Americans, of women, of sexual minorities, of immigrants, are just.

But, paradoxically, so are the grievances of non-elite white men. And these multiple grievances rub each other raw.

Appalachia is the epicenter of declining life spans and living standards for poor and middle class whites. The legitimate demands of the out-groups add to the sense of wounded displacement.

Not surprisingly, this is Trump country. In the Republican primaries, of the 420 counties in the greater Appalachian region, stretching from the southern tier of upstate New York to the Mississippi valley, all but 17 voted for Trump.

The sense of disaffection is so basic that even programs that make a constructive difference, like the positive impact of ObamaCare on Kentucky, are resented rather than welcomed.

In this clash of grievances, one demographic is sitting pretty — very pretty: the economic elite. The grievances of everyone else should be directed against the top.

But Trump's message is mixed. And Hillary is far from an ideal messenger. And Bernie's army has fragmented. So the class coalition against the top doesn't come together.

As a number of commentators, from Alec McGillis to Tom Frank to Arlie Hochschildand J.D. Vance, have observed, the working class sense of displacement is only partly economic. It's partly cultural.

Not only has the modern Democratic presidential party failed to deliver good jobs to working people displaced by the old industrial economy, but it has embraced a blend of cultural liberalism, technocratic boosterism, and education as a silver bullet — a formula that does little for those left behind other than to deepen resentments. To poor whites, the well-heeled elite — Democrat as well as Republican — is living on another planet.

A Clinton Administration, to defeat Trumpism, will have to deliver massive help in the form of good jobs, better prospects for younger Americans, a drastically different trade agenda, a leashing of the one percent and somehow combine that with cultural respect. The more Hillary hopes to do for women, blacks, immigrants and cultural minorities, the more she will need to balance those worthy goals with a politics of class uplift.

Bill Clinton more or less got that complex mix with his 1992 slogan that "people who work hard and play by the rules shouldn't be poor." That line combined an economic message with a cultural one.

But in the 24 years since them, following an abbreviated boom of the late 1990s, economic prospects worsened for many. And the Democratic Party's alliance with Wall Street, producing deregulation and economic collapse, wiped out a lot of the progress that had been made as well as signaling more cultural distance.

Meanwhile, a post-Trump Republican Party will continue its strategy of blockage, leaving grievances to fester and democracy to continue to lose legitimacy. It may detest Trump, but will be doing his work.

And despite recent setbacks, a post-Bernie progressive movement will need to muster all of its strategic smarts, resist the usual circular firing squad, and keep the pressure on for fundamental reform.

If the Democrats do win big on November 8, it's worth about a day of rest and celebration. And then, there is a lot of heavy lifting to do.

-- via my feedly newsfeed

Sunday, August 28, 2016

Saturday, August 27, 2016

Nothing Wrong with Restricting Corporations [feedly]

----

Nothing Wrong with Restricting Corporations

// CEPR Feed

Dean Baker

The Sacramento Bee, August 26, 2016

----

Shared via my feedly newsfeed

Thursday, August 25, 2016

Brexit: A Blow to the Low-Paid? [feedly]

----

Brexit: A Blow to the Low-Paid?

// Economist's View

Chris Dillow:

Brexit: a blow to the low-paid?: The CBI reported today that manufacturers' business confidence has fallen at its fastest rate since early 2009, causing falls in investment and hiring plans. This corroborates surveys by Deloitte, Markit (pdf), the Institute of Directors and, to a lesser extent the Bank of England* all of which suggest that the Brexit vote will depress economic activity. ...

What worries me is that the pain of this will disproportionately hit the low-paid. A new paper (pdf) from the Minneapolis Fed says:

It is precisely the households at the bottom of the wealth distribution with low savings rates and high propensities to consume out of current income that suffer the largest welfare losses from a severe recession. Further, these losses are much more severe than those sustained by the "average" household.

This is because the low-paid have no financial assets to cushion themselves against job loss and so must suffer either big falls in living standards or resort to high-cost payday lenders whereas the rich have savings and/or access to cheaper credit**. Also, firms faced with uncertainty might well respond by hoarding skilled labour – which is harder to find when needed – and trimming unskilled workers.

Although the coming downturn will probably not be as severe as the 2009 one, I suspect that these mechanisms will still operate. ...

What's more, for now we are only seeing the short-run effect of increased uncertainty. In the long-run, it's possible that by depressing world trade growth, the losers from Brexit will be those in more skilled manufacturing and finance jobs.

For now, though, it might be the low-paid that suffer the most from Brexit. These, though, were more likely (pdf) to have voted Leave. We might ask them Johnny Rotten's famous question: ""Ever get the feeling you've been cheated?"

----

Shared via my feedly newsfeed

Great Minds Think Alike [feedly]

----

Great Minds Think Alike

// Crooked Timber

In a pathbreaking ruling, the National Labor Relations Board announced yesterday that graduate student workers at private universities are employees with the right to organize unions.

For three decades, private universities have bitterly resisted this claim. Unions, these universities have argued, would impose a cookie-cutter, one-size-fits-all approach on the ineffably individual and heterogenous nature of graduate education. Unions might be appropriate for a factory, where all the work's the same, but they would destroy the diversity of the academy, ironing out those delicate and delightful idiosyncrasies that make each university what it is. As virtually every elite university now facing an organizing drive of its graduate students is making clear (h/t David Marcus for discovering these particular links).

Here, for example, is Columbia:

What if an individual student objected to a provision in the labor contract? Would he or she still be bound by it?

Yes. Collective bargaining is, by definition, collective in nature. This means that the union speaks and acts for all students in the bargaining unit, and the provisions in the labor contract it negotiates apply to all unit members, unless exceptions and differences are provided for explicitly in the contract.

Here's Yale:

10. What if an individual graduate student disagreed with a provision in the contract? Would he or she still be bound by it?

Yes. Collective bargaining is, as it sounds, collective in nature. That means that the union speaks for all graduate students in the bargaining unit, and the provisions in the contract it negotiates apply to all unit members, unless exceptions and differences are provided for in the agreement.

Here's the University of Chicago:

What if an individual graduate student objected to a provision in the labor contract? Would he or she still be bound by it?

Yes. Collective bargaining is, as it sounds, collectivist in nature. This means that the union speaks and acts for all graduate students in the bargaining unit, and the provisions in the labor contract it negotiates apply to all unit members, unless exceptions and differences are provided for in the contract.

And here's Princeton:

What if an individual graduate student objected to a provision in the labor contract? Would he or she still be bound by it?

Yes. Collective bargaining focuses on graduate students as a group, not as individuals. This means that a union would speak and act for all graduate students in the bargaining unit, and the provisions in the labor contract would apply to all unit members, unless exceptions are provided for in the contract.

Casual readers might conclude that the only thing standardized and cookie-cutter about unions in elite universities is the argument against them.

Or perhaps it's just that great minds sometimes really do think alike.

----

Shared via my feedly newsfeed

Kentucky’s Medicaid Proposal Puts Recent Health Gains at Risk [feedly]

----

Kentucky's Medicaid Proposal Puts Recent Health Gains at Risk

// Center on Budget: Comprehensive News Feed

Kentucky Governor Matt Bevin today submitted a proposal to the Centers for Medicare & Medicaid Services (CMS) that would change the state's Medicaid expansion, leading to tens of thousands of people becoming uninsured. While Gov. Bevin says the changes are necessary to improve Kentuckians' health, research shows that Medicaid expansion has already fueled tremendous improvements in the health of the state's residents.

----

Shared via my feedly newsfeed

Why is President Obama making one last push for the TPP? [feedly]

Even if ALL. Scott's 'facts' are right, it does not mean that, in the absence of trade agreements, things would be ANY better..

----

Why is President Obama making one last push for the TPP?

// Economic Policy Institute Blog

The White House is making one last push for passage of the Trans-Pacific Partnership agreement, most likely during the lame duck session of Congress, after the elections but before the end of the year. This is despite the fact that Democratic presidential nominee Hillary Clinton opposes the TPP, as did Bernie Sanders, her rival in the primary, and as do the majority of Democratic members of Congress.

Let's review the basic facts. Growing imports of goods from low-wage, less-developed countries, which nearly tripled from 2.9 percent of GDP in 1989 to 8.4 percent in 2011 (as shown in Figure A, below), reduced the wages of the typical non-college educated worker in 2011 by "5.5 percent, or by roughly $1,800—for a full-time, full year worker earning the average wage for workers without a four-year college degree," as shown by my colleague Josh Bivens.

Overall, there are nearly 100 million American workers without a 4-year degree. The wage losses suffered by this group likely amount to a full percentage point of GDP—roughly $180 billion per year. Crucially, trade theory and evidence indicate strongly that growing trade redistributes far more income than it creates. The modesty of net benefits from trade is highlighted by the U.S International Trade Commission report that recently estimated that the TPP would generate cumulative net gains of $57.3 billion over the next 16 years, or less than $4 billion per year.

----

Shared via my feedly newsfeed

Fair Pay and Safe Workplaces Executive Order makes contracting system more accountable [feedly]

----

Fair Pay and Safe Workplaces Executive Order makes contracting system more accountable

// Economic Policy Institute Blog

The final rule implementing President Obama's executive order on fair pay and safe workplaces has been issued, along with guidance from the Department of Labor. This is a big deal, affecting as many as 28 million employees in the workforce of hundreds of thousands of government contractors.

The executive order puts in place a commonsense principle: when choosing which companies to do business with, choose the ones that follow the rules rather than the law breakers. Tax dollars should go to contractors with a record of integrity and business ethics, and should not be spent on bad actors. The executive order makes it clear that violations of labor law are an indication of bad ethics and a lack of integrity that must be considered when contracts are awarded.

As part of the contract approval process, federal contractors will have to reveal to the contracting agency any labor law violations they have been found guilty of committing in the previous three years. An agency can refuse to grant a contract to a company that has not resolved its violations. Today, by contrast, it is perfectly normal that a company with several OSHA violations, a National Labor Relations Act violation, and a judgment for wage theft and overtime pay violations could win a $200 million contract from the Department of Transportation or the Defense Department. In fact, the GAO found that almost two-thirds of the 50 largest wage-and-hour violations and almost 40 percent of the 50 largest workplace health-and-safety penalties issued between FY 2005 and FY 2009 were made against companies that went on to receive new government contracts.

----

Shared via my feedly newsfeed

Wednesday, August 24, 2016

Eastern Panhandle Independent Community (EPIC) Radio

John Case has sent you a link to a blog:

Blog: Eastern Panhandle Independent Community (EPIC) Radio

Link: http://www.enlightenradio.org/2016/08/blog-post_24.html

--

Powered by Blogger

https://www.blogger.com/

Blog: Eastern Panhandle Independent Community (EPIC) Radio

Link: http://www.enlightenradio.org/2016/08/blog-post_24.html

--

Powered by Blogger

https://www.blogger.com/

Eastern Panhandle Independent Community (EPIC) Radio

John Case has sent you a link to a blog:

Its happening again: The are you crazy show on EPIC Radio

Blog: Eastern Panhandle Independent Community (EPIC) Radio

Link: http://www.enlightenradio.org/2016/08/its-are-you-crazy-show-on-epic-radio.html

--

Powered by Blogger

https://www.blogger.com/

Its happening again: The are you crazy show on EPIC Radio

Blog: Eastern Panhandle Independent Community (EPIC) Radio

Link: http://www.enlightenradio.org/2016/08/its-are-you-crazy-show-on-epic-radio.html

--

Powered by Blogger

https://www.blogger.com/

Tuesday, August 23, 2016

The economist: Big Idea #5 Nash Equilibrium

Big Idea #5

http://gregmankiw.blogspot.com/2016/08/big-idea-5.html

-- via my feedly newsfeed

http://gregmankiw.blogspot.com/2016/08/big-idea-5.html

Prison breakthrough

The fifth of our series on seminal economic ideas looks at the Nash equilibrium

JOHN NASH arrived at Princeton University in 1948 to start his PhD with a one-sentence recommendation: "He is a mathematical genius". He did not disappoint. Aged 19 and with just one undergraduate economics course to his name, in his first 14 months as a graduate he produced the work that would end up, in 1994, winning him a Nobel prize in economics for his contribution to game theory.

On November 16th 1949, Nash sent a note barely longer than a page to the Proceedings of the National Academy of Sciences, in which he laid out the concept that has since become known as the "Nash equilibrium". This concept describes a stable outcome that results from people or institutions making rational choices based on what they think others will do. In a Nash equilibrium, no one is able to improve their own situation by changing strategy: each person is doing as well as they possibly can, even if that does not mean the optimal outcome for society. With a flourish of elegant mathematics, Nash showed that every "game" with a finite number of players, each with a finite number of options to choose from, would have at least one such equilibrium.

His insights expanded the scope of economics. In perfectly competitive markets, where there are no barriers to entry and everyone's products are identical, no individual buyer or seller can influence the market: none need pay close attention to what the others are up to. But most markets are not like this: the decisions of rivals and customers matter. From auctions to labour markets, the Nash equilibrium gave the dismal science a way to make real-world predictions based on information about each person's incentives.

One example in particular has come to symbolise the equilibrium: the prisoner's dilemma. Nash used algebra and numbers to set out this situation in an expanded paper published in 1951, but the version familiar to economics students is altogether more gripping. (Nash's thesis adviser, Albert Tucker, came up with it for a talk he gave to a group of psychologists.)

It involves two mobsters sweating in separate prison cells, each contemplating the same deal offered by the district attorney. If they both confess to a bloody murder, they each face ten years in jail. If one stays quiet while the other snitches, then the snitch will get a reward, while the other will face a lifetime in jail. And if both hold their tongue, then they each face a minor charge, and only a year in the clink (see diagram).

There is only one Nash-equilibrium solution to the prisoner's dilemma: both confess. Each is a best response to the other's strategy; since the other might have spilled the beans, snitching avoids a lifetime in jail. The tragedy is that if only they could work out some way of co-ordinating, they could both make themselves better off.

The example illustrates that crowds can be foolish as well as wise; what is best for the individual can be disastrous for the group. This tragic outcome is all too common in the real world. Left freely to plunder the sea, individuals will fish more than is best for the group, depleting fish stocks. Employees competing to impress their boss by staying longest in the office will encourage workforce exhaustion. Banks have an incentive to lend more rather than sit things out when house prices shoot up.

Crowd trouble

The Nash equilibrium helped economists to understand how self-improving individuals could lead to self-harming crowds. Better still, it helped them to tackle the problem: they just had to make sure that every individual faced the best incentives possible. If things still went wrong—parents failing to vaccinate their children against measles, say—then it must be because people were not acting in their own self-interest. In such cases, the public-policy challenge would be one of information.

Nash's idea had antecedents. In 1838 August Cournot, a French economist, theorised that in a market with only two competing companies, each would see the disadvantages of pursuing market share by boosting output, in the form of lower prices and thinner profit margins. Unwittingly, Cournot had stumbled across an example of a Nash equilibrium. It made sense for each firm to set production levels based on the strategy of its competitor; consumers, however, would end up with less stuff and higher prices than if full-blooded competition had prevailed.

Another pioneer was John von Neumann, a Hungarian mathematician. In 1928, the year Nash was born, von Neumann outlined a first formal theory of games, showing that in two-person, zero-sum games, there would always be an equilibrium. When Nash shared his finding with von Neumann, by then an intellectual demigod, the latter dismissed the result as "trivial", seeing it as little more than an extension of his own, earlier proof.

In fact, von Neumann's focus on two-person, zero-sum games left only a very narrow set of applications for his theory. Most of these settings were military in nature. One such was the idea of mutually assured destruction, in which equilibrium is reached by arming adversaries with nuclear weapons (some have suggested that the film character of Dr Strangelove was based on von Neumann). None of this was particularly useful for thinking about situations—including most types of market—in which one party's victory does not automatically imply the other's defeat.

Even so, the economics profession initially shared von Neumann's assessment, and largely overlooked Nash's discovery. He threw himself into other mathematical pursuits, but his huge promise was undermined when in 1959 he started suffering from delusions and paranoia. His wife had him hospitalised; upon his release, he became a familiar figure around the Princeton campus, talking to himself and scribbling on blackboards. As he struggled with ill health, however, his equilibrium became more and more central to the discipline. The share of economics papers citing the Nash equilibrium has risen sevenfold since 1980, and the concept has been used to solve a host of real-world policy problems.

One famous example was the American hospital system, which in the 1940s was in a bad Nash equilibrium. Each individual hospital wanted to snag the brightest medical students. With such students particularly scarce because of the war, hospitals were forced into a race whereby they sent out offers to promising candidates earlier and earlier. What was best for the individual hospital was terrible for the collective: hospitals had to hire before students had passed all of their exams. Students hated it, too, as they had no chance to consider competing offers.

Despite letters and resolutions from all manner of medical associations, as well as the students themselves, the problem was only properly solved after decades of tweaks, and ultimately a 1990s design by Elliott Peranson and Alvin Roth (who later won a Nobel economics prize of his own). Today, students submit their preferences and are assigned to hospitals based on an algorithm that ensures no student can change their stated preferences and be sent to a more desirable hospital that would also be happy to take them, and no hospital can go outside the system and nab a better employee. The system harnesses the Nash equilibrium to be self-reinforcing: everyone is doing the best they can based on what everyone else is doing.

Other policy applications include the British government's auction of 3G mobile-telecoms operating licences in 2000. It called in game theorists to help design the auction using some of the insights of the Nash equilibrium, and ended up raising a cool £22.5 billion ($35.4 billion)—though some of the bidders' shareholders were less pleased with the outcome. Nash's insights also help to explain why adding a road to a transport network can make journey times longer on average. Self-interested drivers opting for the quickest route do not take into account their effect of lengthening others' journey times, and so can gum up a new shortcut. A study published in 2008 found seven road links in London and 12 in New York where closure could boost traffic flows.

Game on

The Nash equilibrium would not have attained its current status without some refinements on the original idea. First, in plenty of situations, there is more than one possible Nash equilibrium. Drivers choose which side of the road to drive on as a best response to the behaviour of other drivers—with very different outcomes, depending on where they live; they stick to the left-hand side of the road in Britain, but to the right in America. Much to the disappointment of algebra-toting economists, understanding strategy requires knowledge of social norms and habits. Nash's theorem alone was not enough.

A second refinement involved accounting properly for non-credible threats. If a teenager threatens to run away from home if his mother separates him from his mobile phone, then there is a Nash equilibrium where she gives him the phone to retain peace of mind. But Reinhard Selten, a German economist who shared the 1994 Nobel prize with Nash and John Harsanyi, argued that this is not a plausible outcome. The mother should know that her child's threat is empty—no matter how tragic the loss of a phone would be, a night out on the streets would be worse. She should just confiscate the phone, forcing her son to focus on his homework.

Mr Selten's work let economists whittle down the number of possible Nash equilibria. Harsanyi addressed the fact that in many real-life games, people are unsure of what their opponent wants. Economists would struggle to analyse the best strategies for two lovebirds trying to pick a mutually acceptable location for a date with no idea of what the other prefers. By embedding each person's beliefs into the game (for example that they correctly think the other likes pizza just as much as sushi), Harsanyi made the problem solvable.A different problem continued to lurk. The predictive power of the Nash equilibrium relies on rational behaviour. Yet humans often fall short of this ideal. In experiments replicating the set-up of the prisoner's dilemma, only around half of people chose to confess. For the economists who had been busy embedding rationality (and Nash) into their models, this was problematic. What is the use of setting up good incentives, if people do not follow their own best interests?

All was not lost. The experiments also showed that experience made players wiser; by the tenth round only around 10% of players were refusing to confess. That taught economists to be more cautious about applying Nash's equilibrium. With complicated games, or ones where they do not have a chance to learn from mistakes, his insights may not work as well.

The Nash equilibrium nonetheless boasts a central role in modern microeconomics. Nash died in a car crash in 2015; by then his mental health had recovered, he had resumed teaching at Princeton and he had received that joint Nobel—in recognition that the interactions of the group contributed more than any individual.

LAST IN THIS SERIES:

• The Mundell-Fleming trilemma

-- via my feedly newsfeed

IMF Cannot Quit Fiscal Consolidation (in Asian Surplus Countries) [feedly]

IMF Cannot Quit Fiscal Consolidation (in Asian Surplus Countries)

http://economistsview.typepad.com/economistsview/2016/08/imf-cannot-quit-fiscal-consolidation-in-asian-surplus-countries.html

-- via my feedly newsfeed

http://economistsview.typepad.com/economistsview/2016/08/imf-cannot-quit-fiscal-consolidation-in-asian-surplus-countries.html

Brad Setser:

IMF Cannot Quit Fiscal Consolidation (in Asian Surplus Countries): In theory, the IMF now wants current account surplus countries to rely more heavily on fiscal stimulus and less on monetary stimulus.

This shift makes sense in a world marked by low interest rates, the risk that surplus countries will export liquidity traps to deficit economies, and concerns aboutcontagious secular stagnation. Fiscal expansion tends to lower the surplus of surplus countries and regions, while monetary expansion tends to increase surpluses.

And large external surpluses should be a concern in a world where imbalances in goods trade are once again quite large—though the goods surpluses now being chalked up in many Asian countries are partially offset by hard-to-track deficits in "intangibles" (to use an old term), notably China's ongoing deficit in investment income and its ever-rising and ever-harder-to-track deficit in tourism.

In practice, though, the Fund seems to be having trouble actually advocating fiscal expansion in any major economy with a current account surplus.

Best I can tell, the Fund is encouraging fiscal consolidation in China, Japan, and the eurozone. These economies have a combined GDP of close to $30 trillion. The Fund, by contrast, is, perhaps, willing to encourage a tiny bit of fiscal expansion in Sweden (though that isn't obvious from the 2015 staff report) and in Korea—countries with a combined GDP of $2 trillion.*

I previously have noted that the Fund is advocating a 2017 fiscal consolidation for the eurozone, as the consolidation the Fund advocates in France, Italy, and Spain would overwhelm the modest fiscal expansion the Fund proposed in the Netherlands (Germany would remain on the fiscal sidelines per the IMF's recommendation).

The same seems to be true in East Asia's main surplus economies. ...

Bottom line: if the Fund wants fiscal expansion in surplus countries to drive external rebalancing and reduce current account surpluses, it actually has to be willing to encourage major countries with large external surpluses to do fiscal expansion. Finding limited fiscal space in Sweden and perhaps Korea won't do the trick. 20 or 30 basis points of fiscal expansion in small economies won't move the global needle. Not if China, Japan, and the eurozone all lack fiscal space and all need to consolidate over time.

-- via my feedly newsfeed

Subscribe to:

Posts (Atom)

-

John Case has sent you a link to a blog: Blog: Eastern Panhandle Independent Community (EPIC) Radio Post: Are You Crazy? Reall...

-

via Bloomberg -- excerpted from "Balance of Power" email from David Westin. Welcome to Balance of Power, bringing you the late...

via Bloomberg -- excerpted from "Balance of Power" email from David Westin. Welcome to Balance of Power, bringing you the late... -

---- Mylan's EpiPen profit was 60% higher than what the CEO told Congress // L.A. Times - Business Lawmakers were skeptical last...