http://blogs.cfr.org/setser/2016/06/29/post-brexit/

A few thoughts, focusing on narrow issues of macroeconomic management rather than the bigger political issues.

The U.K. has been running a sizeable current account deficit for some time now, thanks to an unusually low national savings rate. That means, on net, it has been supplying the rest of Europe with demand—something other European countries need. This isn't likely to provide Britain the negotiating leverage the Brexiters claimed (the other European countries fear the precedent more than the loss of demand) but it will shape the economic fallout.

The fall in the pound is a necessary part of the U.K.'s adjustment. It will spread the pain from a downturn in British demand to the rest of the euro area. Brexit uncertainty is thus a sizable negative shock to growth in Britian's euro area trading partners not just to Britain itself: relative to the pre-Brexit referendum baseline, I would guess that Brexit uncertainty will knock a cumulative half a percentage point off euro area growth over the next two years.*

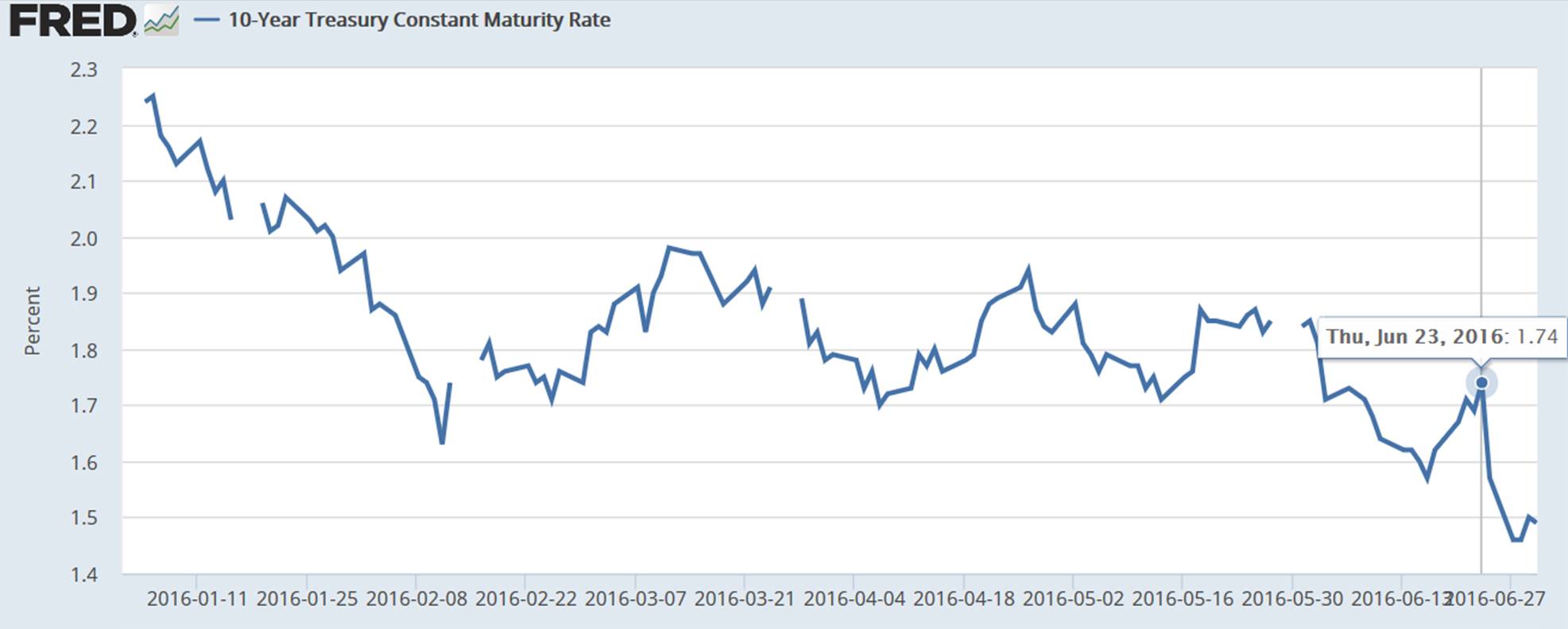

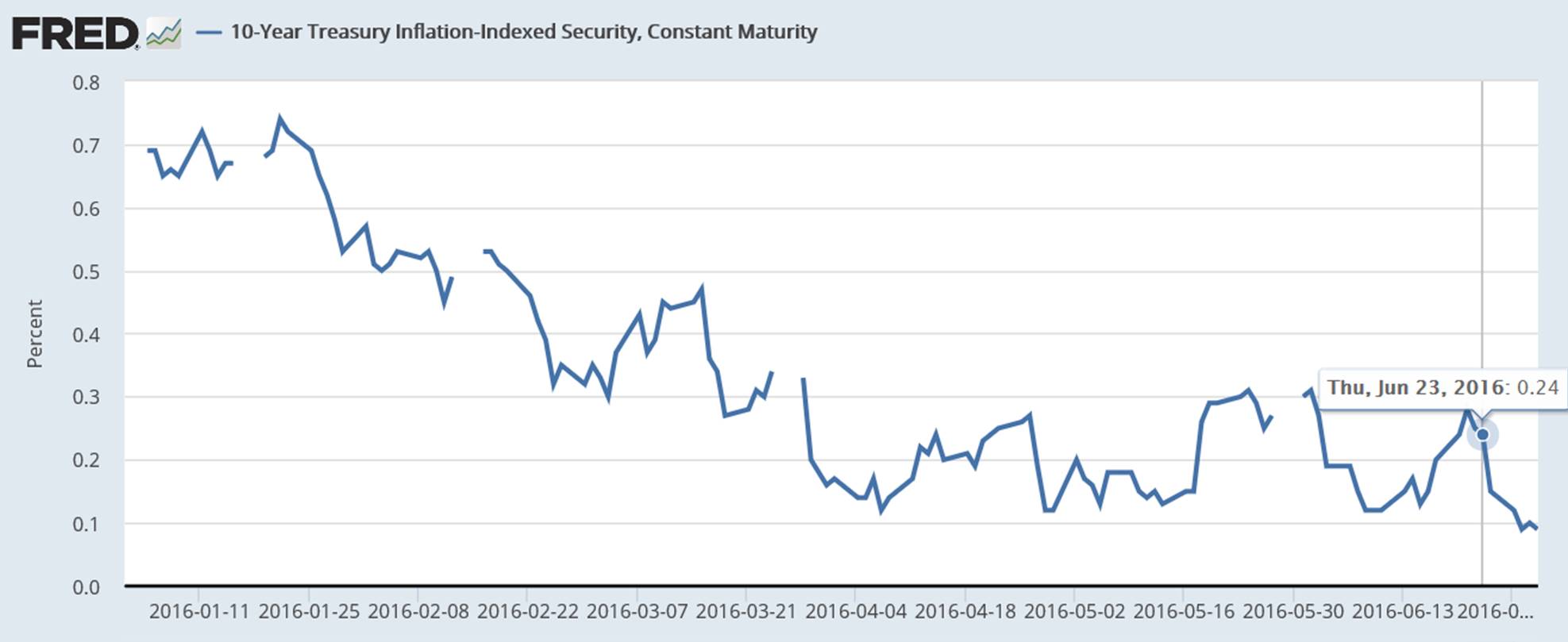

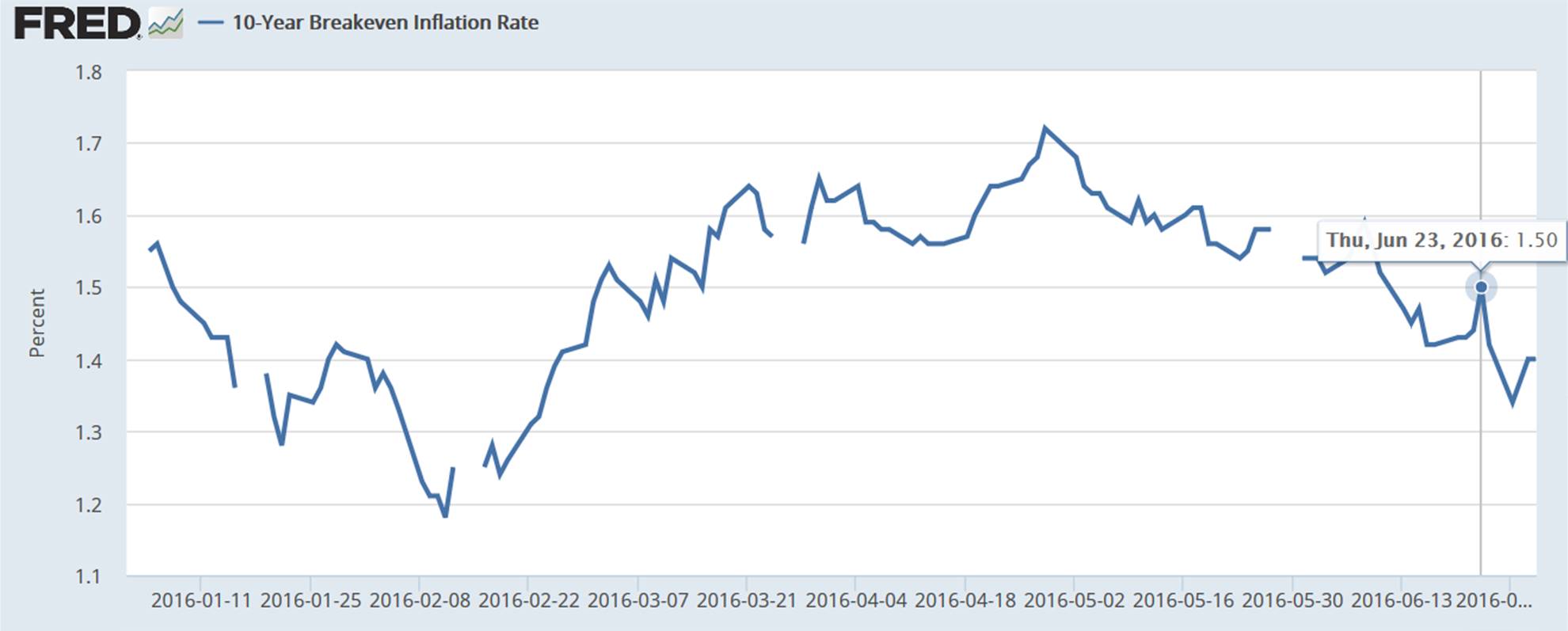

Of course, the euro area, which runs a significant current account surplus and can borrow at low nominal rates, has fiscal capacity to counteract this shock. Germany is being paid to borrow for ten years, and the average ten year rate for the euro area as a whole is around 1 percent. The euro area could provide a fiscal offset, whether jointly, through new euro area investment funds or simply through a shift in say German policy on public investment and other adjustments to national policy.

I say this knowing full-well the political constraints to fiscal action. The Germans do not want to run a deficit. The Dutch are committed to bringing an already low deficit down further. France, Italy and especially Spain face pressure from the Commission to tighten policy. The Juncker plan never really created the capacity for shared funding of investment. The euro area's aggregate fiscal stance is, more or less, the sum of national fiscal policies of the biggest euro area economies.

If I had to bet, I would bet that the euro area's aggregate fiscal impulse will be negative in 2017—exactly the opposite of what it should be when a surplus region is faced with a shock to external demand. A lot depends on the fiscal path Spain negotiates once it forms a new government, given that is running the largest fiscal deficit of the euro area's big five economies.

Economically, the euro area would also benefit from additional focus on the enduring overhang of private debt, and the non-performing loans that continue to clog the arteries of credit. Debt overhangs in the private sector—Dutch mortgage debt, Portuguese corporate debt, Italian small-business loans—are one reason why euro area demand growth has lagged.

Euro area banks should have been recapitalized years ago, with public money if needed, to allow more scope for the write down of private debt. But in key countries they were not, even with the impetus from various stress tests and the move toward (limited) banking union. And Europe's new banking rules are now creating additional incentives for delay.

The banking rules require bail-ins, which are typically better politics than outright bail-outs.

But countries like Italy are caught in a bind:

• Clearing away legacy non-performing loans (NPLs) takes capital—capital many of its banks do not have;

• National governments cannot provide public capital without bailing in a portion of the banks' liabilities structure;

• And in Spain, Portugal and Italy, many of the banks that need capital now raised capital in the past by selling preferred equity and subordinated debt to their own depositors, so bail-ins in effect means hitting small investors who took on a set of risks they didn't understand (and often made investments before the banking rules were tightened).

The consensus VoXEU document alluded to this problem, but didn't quite spell out how the current banking rules could be "credibly modified."

Putting public funds into the banks does not addresses popular concerns about the way the global economy works. Forcing retail investors to take losses in the name of new European rules does not obviously build public support for "more" Europe. Keeping bad loans at inflated marks on the balance sheet of weak banks undermines new lending, and makes it hard for private demand growth to offset the impact of fiscal consolidation. There is no cost-free option, economically or politically.

The euro area's ongoing banking issues highlight the broader tensions created by a conception of the euro area that focuses on the application of common rules with only modest sharing of fiscal risks—and by a political process that has often designed those rules a bit too restrictively, with too much deference to Germany's desire to avoid being stuck with other countries' bills and too little recognition of the need to allow the member countries to use their own national balance sheets to spur growth.

Something will need to give, eventually.

* My back-of-the envelope estimate is close to Draghi's estimate, and similar to that ofGoldman. The OECD's estimate actually suggest a slightly bigger impact on the euro area from a similar to slighter larger fall in British output. In their model, the euro area is facing a two year drag on growth of about a percentage point; see p. 22.

-- via my feedly newsfeed