https://equitablegrowth.org/the-coronavirus-recession-is-an-opportunity-to-cancel-all-u-s-student-loan-debt/

This past March, as a coronavirus relief measure, Congress suspended payments on a lion's share of federally owned student loans for 6 months. When this temporary loan forbearance expires on September 30, it should be extended—permanently.

Many borrowers will not be prepared to begin making payments that soon. But more importantly, none of these student loan borrowers should ever have to make another payment. Cancelling these debts would benefit the U.S. economy, reduce the massive racial wealth divide, and create new opportunities for a generation of college graduates whose hopes the economy has wiped out twice in a dozen years.

The Coronavirus Aid, Relief, and Economic Security, or CARES Act places federal student loans in administrative forbearance. That means debtors still owe their full debt but need not make any payments, and no interest will accrue on the loan during this period. It's a good idea to provide relief to the more than 40 million borrowers in our country, many of whom face staggering levels of debts, not to mention helping to sustain an otherwise bleak economy by putting some money in the pockets of consumers.

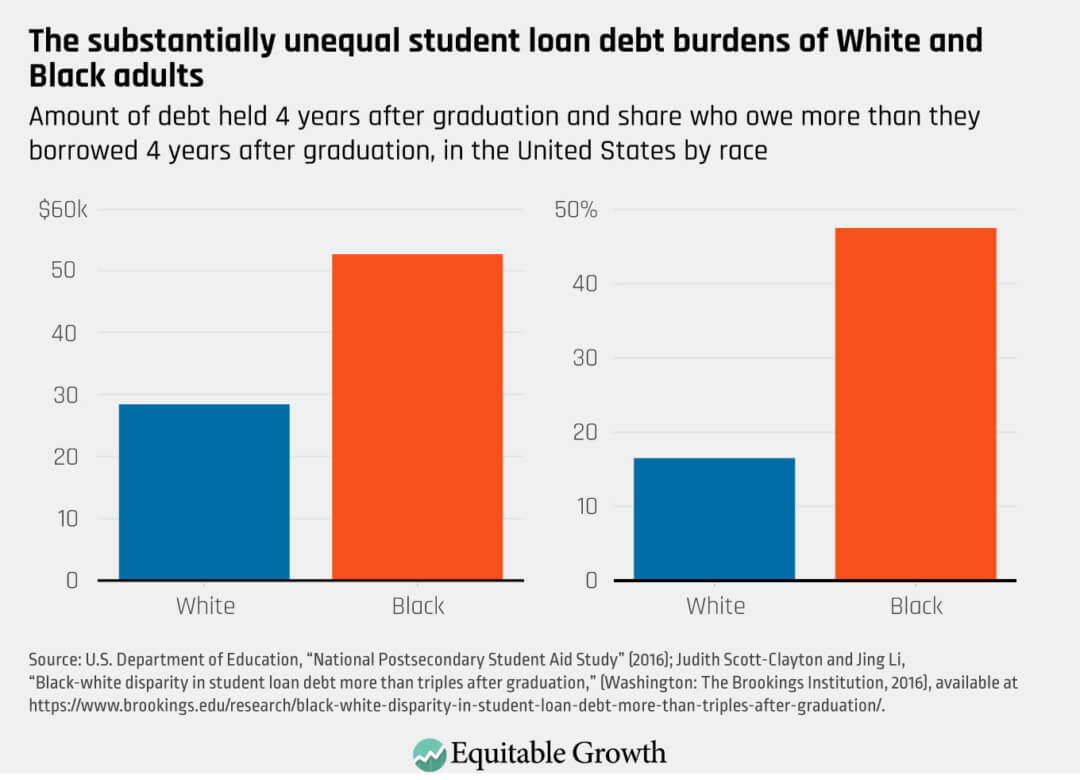

But this measure doesn't go nearly far enough. This debt should not merely be suspended but cancelled entirely. Even before the coronavirus pandemic, federal student loan debt was crushing the financial and career aspirations of millions of borrowers. With college costs consistently rising faster than inflation and federal grant aid to students not keeping up, the aggregate amount of student debt is more than triple its level just 13 years ago—revealing the systemic nature of the trap created by a system of debtor's education. Debt levels are especially high for Black students, who, 4 years after graduation, have an average obligation of more than $50,000, compared to less than $30,000 for the average White student. (See Figure 1.)

Figure 1

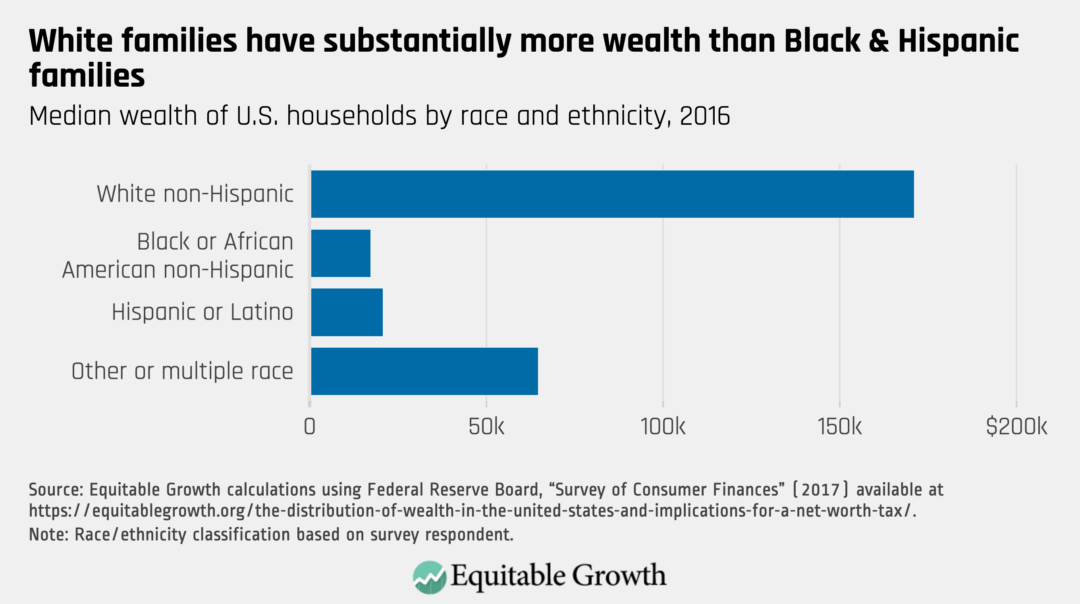

This higher debt load stems, in part, from the extraordinary gap in wealth between White and Black families. The median White household has 10 times the assets of the average Black family. (See Figure 2.)

Figure 2

Receiving less protection from parental wealth, Black students take on higher debt loads. Then, upon entering the labor market as young adults, these students face a harder time paying off their loans in a labor market characterized by racial discrimination. Evidence suggests that student debt has significant social impacts on the most vulnerable borrowers, including impeded family formation and poorer mental health. While student debt has conventionally been thought of as "good debt," the investment generates widely disparate rates of return by race, given the prevailing social framework of unequal housing and Kindergarten through 12th grade education, predatory finance, and labor market discrimination.

The past decade and a half were especially cruel to college graduates. The scarring effect of the Great Recession of 2007–2009 is well-known. Those who graduated during that recession and immediately after will, on average, earn less throughout their careers. Yet, in part because of legislation permitting higher federal student borrowing, overall student borrowing began to skyrocket, surpassing credit card debt for the first time in 2010.

In addition, during the Great Recession, adults were encouraged to wait out the poor labor market and advance their career prospects by furthering their education. Many accrued more student loan debt but not all returned to the workforce with a degree or with the substantial improvement in earnings potential needed to pay off their debt. College costs are continuing to rise faster than overall inflation and federal grant aid is lagging, causing a significant portion of the millennial generation and its immediate successors to pursue adult lives with a millstone around their necks.

Cancelling student debt during the coronavirus recession and going forward with tution-free universities would provide the greatest benefit to those who are suffering the most today. It is well-documented that people of color are contracting and dying from COVID-19 in numbers far out of proportion to their share of the population. Those service-sector jobs that don't require a college degree, where Black workers and immigrants are overrepresented, are also less likely to provide access to insurance coverage or paid sick leave than other sectors. As the saying goes, when America gets a cold, Black people get the flu, but when America gets the flu, Black folks are far more likely to die. The anger we are seeing on the streets of cities across the nation is due not only to the violence imposed on Black Americans by discriminatory law enforcement but also is inextricably intertwined with social, educational, and economic injustices all created by the same society.

The concept of cancelling federal student debt is not a new one. Congress enacted loan forgiveness programs with Presidents George W. Bush and Barack Obama. The Bush program, initiated in 2007, focused on teachers and other public servants, as well as those working for nonprofit organizations, but it is exceedingly complex. Since loans became eligible for forgiveness in 2017, fewer than 3,400 borrowers have been approved for forgiveness, though nearly 200,000 have applied.

The Obama plan, which began in 2010, aimed at a far broader swath of borrowers. It enables borrowers to make payments based on a percentage of income. It also allows for cancellation of loans, but only after 20–25 years of payment. It is too early to tell how many borrowers will be aided by the cancellation element of the program, but, as with the Bush program, the Trump administration is showing that much can be done through administrative efforts to undermine this program's intent by making it difficult for borrowers to qualify.

Cancellation of student debt was among the focal points of the recent Democratic Party presidential nomination campaigns. While some presidential candidates supported full student debt cancellation, former Vice President Joe Biden recently made a more modest proposal to forgive all undergraduate loan debt for borrowers who attended public colleges and universities, as well as historically Black colleges and universities, private minority-serving institutions, and for-profit colleges that disproportionately enroll Black students. Only those earning up to $125,000 would be eligible for forgiveness. In addition, Vice President Biden supports $10,000 in across-the-board loan forgiveness as a response to the coronavirus crisis.

There's no question this proposal goes a long way and would cancel the loans of many millions of borrowers. Loan forgiveness, however, must be complete. Partial proposals—whether they limit the amount of cancellation, limit the source of debt to undergraduates, establish income ceilings, or distinguish between public and private institutions—leave us with the same mess of rules, income verification, and administrative burdens plaguing the previous, wildly ineffective attempts and will not protect young Black people seeking to use education as a tool for social mobility. Partial forgiveness would keep in place the unfair burden carried by this generation of borrowers, who were hit hard by higher debt and a double whammy of now-two recessions. Full cancellation is simple. It doesn't pose administrative barriers, and it avoids the stigma associated with means testing.

Moreover, full cancellation leads naturally to what we consider to be the logical next step. Once Congress cancels all student debt, it should not stop there. Just as free public elementary education has effectively been a universal (though unevenly applied) economic right since the 19th century, free higher education should become the standard in the 21st century. Most young people have little choice but to pursue a college education if they wish to raise their socioeconomic standing beyond where they started out in life. And for many, higher education is a necessary step to earning a living wage. Providing tuition-free public higher education to all Americans would eliminate the social and psychological stigma associated with the current system of financial aid and eliminate the need for future generations to carry burdensome debts.

The coronavirus pandemic, the ensuing recession, and the community response to the police killing of George Floyd and far too many other Black Americans in 2020 and beyond bring into sharp focus the barriers American society places in front of today's generation of Black students—barriers as old as our nation that continue to this day. Student loan debt exacerbates the challenges facing young Black Americans trying to establish careers and begin families. Eliminating this debt would be an important step toward reducing racial and economic inequality in the United States and bringing about the globally competitive, educated workforce that will unleash the country's overall productive potential. As Congress and American voters facing a presidential election think about big solutions to America's very big problems, this is one of the most important and effective actions we can consider.

-- via my feedly newsfeed

No comments:

Post a Comment