https://lanekenworthy.net/2019/11/21/whats-the-best-type-of-healthcare-system/

If we're going to improve our healthcare system, it's worth looking closely at the experiences of other rich democratic countries. There are two principal types. They're sometimes referred to as the Beveridge model and the Bismarck model. I'll label them "single payer" and "insurance funds."1

Single payer systems

In this type of system, the government pays providers (from tax revenues), decides prices, decides what procedures are covered, decides copayments, and more. It also runs some or most of the hospitals and employs some or most of the medical providers. The best-known example of this type of system is the United Kingdom's National Health Service (NHS).

Health care is paid for via taxes. Britons don't pay health insurance premiums. There are no copayments for diagnosis and treatment, whether for a visit to the doctor or specialized surgery. There is a small copayment for medicines, but it is waived for the elderly, people with chronic conditions, and other needy groups.

A government agency draws on available research to decide what treatments and medications are sufficiently effective and affordable to justify coverage. Some basic things, like eyeglasses and some types of dental care, aren't covered. Patients must see their general practitioner first and get a referral in order to see a specialist, much like with HMOs in the United States. Patients can see any general practitioner of their choosing, and once they get a referral they can choose which specialist to see next.

How is cost control achieved? The key is that a single agency decides what tests, procedures, and medicines will be covered and how much providers will be paid. In addition, administrative costs are very low because there are no disputes about eligibility, there is a single set of rules, and there is a single price list.

General practitioners are paid based on the number of patients they have ("capitation"), not the number of patient visits or the number of tests and procedures they perform or the number of referrals they make to specialist doctors. Most general practitioners in the UK aren't government employees. Formally, they are self-employed doctors who contract with the government. But this is a distinction that makes little difference, as what they can do and how much they can charge are determined by the NHS. Doctors can provide private medical care on the side, charging what they like. But the private market is utilized by a small minority of Britons; 90% use only the NHS for their health care.

Britons pay for health care via their taxes and some small copayments. And if they want to avoid waiting to see a specialist or for a "nonessential" procedure, or if they'd like to get a procedure that isn't covered by the NHS, they pay out of pocket.

Among the world's rich longstanding-democratic nations, Australia, Canada, Ireland, New Zealand, Italy, Portugal, Spain, Denmark, Finland, Norway, Sweden, and South Korea have healthcare systems that are broadly similar to the British one. The United States does too; about 40% of Americans get their health care via Medicare (elderly), Medicaid (low income), the Veterans Administration (former military), or the Military Health System (current military). So this is the type of system favored by the English-speaking nations, the southern European countries, the Nordic countries, and most recently South Korea.

There are differences among these countries — whether or not medical providers are formally government employees, what tests and procedures are covered (two out of three nonelderly Canadians have private insurance to supplement the government package), whether patients must see a primary-care physician first or can go straight to a specialist, how much choice patients have about doctors and hospitals, the existence and size of copayments and deductibles, whether the key decisions are made mostly by a central government agency (UK) or by local governments (Canada, Denmark, Italy, Sweden), whether private health insurance can cover the same procedures as the public system (in Canada and Italy it can't), and more. But the basic structure is the same: government decides what tests, procedures, and medicines are covered, how much providers are paid, and where the money comes from (taxes, copayments, something else).

In this type of system, these matters are political decisions. If citizens aren't satisfied with their access to medical care, with its quality, with waiting times, or with the amount of taxes they're paying to fund it, they can lobby the government to make changes or vote in a new government that will do so.

Insurance funds systems

Austria, Belgium, France, Germany, Japan, Netherlands, and Switzerland — the affluent continental European nations plus Japan — organize healthcare differently. Health insurers, usually referred to as insurance funds, are the principal payers. Citizens pick an insurance fund and pay a fee, often supplemented by a payment from their employer. The insurance fund determines what tests, procedures, and medications will be covered. Hospitals and doctors are mostly nonprofit or private; relatively few are administered or employed by the government.

In this respect, things work similarly to the way they do for a majority of working-age Americans who get health insurance through an employer-sponsored plan and get treated by nonprofit or private physicians and hospitals. But there the similarity ends. First, everyone is covered. Individuals typically are required to purchase health insurance through an insurance fund, and those who don't or can't are either assigned to a fund or are covered by the government. The insurance funds must accept all applicants; they can't refuse coverage on grounds of age, risk, preexisting conditions, or for any other reason. Second, there is a basic plan that all insurers must offer at a fixed price. Typically they also can offer better plans, which cover more services or allow more choice among doctors or shorter waits, at a higher price. Third, prices are tightly controlled. Sometimes, as in France and Japan, government sets the prices in consultation with representatives of hospitals and doctors. In other countries, such as Germany and the Netherlands, prices are determined, for the nation as a whole, via bargaining between representatives of the insurance funds and representatives of medical providers. If those negotiations break down, government steps in to impose a resolution. Fourth, insurance funds can't be for-profit. (They do compete with one another, though.)

There are differences across these countries. The number of funds varies: France has about 15, Germany 120, Japan 3,400. People can choose to join whatever insurance fund they like in most of these nations, but in France they must go with the one set up for their line or work or the region where they live, and they stay with that fund for life, even if they move across the country or lose their job. Japanese must go with their employer's fund. In some nations people can switch between funds on short notice (Germany, Switzerland), whereas in others switching can only be done once a year (Netherlands). In some countries patients can go to whatever doctor or hospital they like (France, Japan), while in others they must first see a primary-care physician. Copayments and deductibles vary. In some of these countries, lots of people purchase supplementary private insurance to cover things the insurance plan doesn't (90% of the working-aged in France, 84% of the population in the Netherlands). In Germany, but not in most other countries, the affluent (about 7% of the population) are allowed to opt out of this system and purchase private insurance on their own.

Using employer payments as a major source of financing for health care seems outdated. In a society where people switch jobs frequently, it makes little sense for insurance against a potentially major and very costly risk to be tied to one's employer. Moreover, providing health insurance is expensive for firms, putting them at a disadvantage relative to foreign competitors. And it likely acts as a brake on wage increases. Nevertheless, employer-based health insurance seems to work reasonably well in these insurance funds countries. An important reason why is that if people quit or lose their job, they are automatically kept with their existing insurance fund or switched into a government health insurance plan. And the cost of health care is contained, so it's less of a burden for employers.

Which type of system works better?

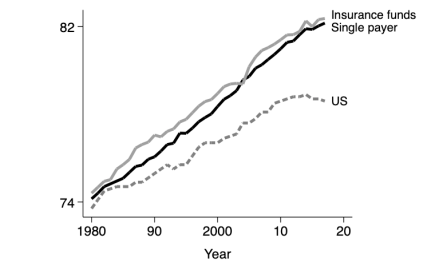

Figure 1 shows average life expectancy since 1980 in the twelve rich democratic countries that have a single-payer system and the seven countries that have an insurance fund system.2 There is no meaningful difference between them.

Figure 1. Life expectancy by type of healthcare system

Years of life expectancy at birth. The vertical axis doesn't begin at zero. The "single payer" countries are Australia, Canada, Denmark, Finland, Ireland, Italy, New Zealand, Norway, Portugal, Spain, Sweden, and the United Kingdom. The "insurance funds" countries are Austria, Belgium, France, Germany, Japan, Netherlands, and Switzerland. Data source: OECD.

Life expectancy is influenced not only by a nation's healthcare system but also by lifestyle, diet, education, affluence, violence, and more. A measure that more directly gets at the impact of the healthcare system on longevity is "avoidable deaths," defined as deaths among persons aged 0 to 74 from diseases or conditions that are treatable or that could have been prevented through better public health interventions. Comparable data are available only for European nations and only for recent years. This includes nine countries with a single-payer system (Denmark, Finland, Ireland, Italy, Norway, Portugal, Spain, Sweden, and the United Kingdom) and six countries with an insurance-funds system (Austria, Belgium, France, Germany, the Netherlands, and Switzerland). As we see in figure 2, the avoidable death rate is virtually identical across the two system types.

Figure 2. Avoidable death rate by type of healthcare system

Per 100,000 persons aged 0 to 74. Deaths from diseases or conditions that are treatable ("treatable" deaths) plus deaths that could have been prevented through better public health interventions ("preventable" deaths). The vertical axis doesn't begin at zero. The "single payer" countries are Denmark, Finland, Ireland, Italy, Norway, Portugal, Spain, Sweden, and the United Kingdom. The "insurance funds" countries are Austria, Belgium, France, Germany, Netherlands, and Switzerland. Data source: Eurostat, "Preventable and Treatable Mortality Statistics."

Figure 3 shows health expenditures as a share of GDP. Here we see a slight advantage for single-payer countries, and that advantage increases a bit over time. It may be that this is due to greater efficiency — for instance, lower administrative costs or less waste. Then again, it could be a result of political choices to cover fewer procedures or medications, which might result in longer wait times or less use of medical care. We lack data that would permit the sort of detailed comparison we need in order to reach a confident conclusion about the sources of this difference in health expenditures.

Figure 3. Health expenditures by type of healthcare system

Share of GDP. Total (public plus private) expenditures. The "single payer" countries are Australia, Canada, Denmark, Finland, Ireland, Italy, New Zealand, Norway, Portugal, Spain, Sweden, and the United Kingdom. The "insurance funds" countries are Austria, Belgium, France, Germany, Japan, Netherlands, and Switzerland. Data source: OECD.

In 2013 and 2016, the Commonwealth Fund conducted thorough assessments of the healthcare systems of eleven of these countries. They included six countries with a single-payer system (Australia, Canada, New Zealand, Norway, Sweden, and the United Kingdom) and four with an insurance-funds system (France, Germany, the Netherlands, and Switzerland), along with the United States. They scored each nation in five areas — care process (preventive care, safe care, coordinated care, and engagement and patient preferences), access (affordability and timeliness), administrative efficiency, equity, and healthcare outcomes — and they used these scores to determine an overall ranking.

Figure 4 shows the countries' ranking in each year along with the averages for the two groups. In 2013 the average rank for countries with a single-payer system was exactly the same as the average for countries with an insurance-funds system. In 2016 the average ranking was better for single-payer countries than for insurance-fund countries. But the difference was small — small enough that it easily could disappear if more nations from each group were included. It might also be a product of error; while these assessments are careful and thorough, that doesn't mean they are perfectly accurate.

Figure 4. Healthcare system performance rank by type of healthcare system

The rankings are for 2013 and 2016. Data sources: Karen Davis, Kristof Stremikis, David Squires, and Cathy Schoen, "Mirror, Mirror on the Wall: How the Performance of the U.S. Health Care System Compares Internationally," Commonwealth Fund, 2014, exhibit 2; Eric C. Schneider, Dana O. Sarnak, David Squires, Arnav Shah, and Michelle M. Doty, "Mirror, Mirror 2017: International Comparison Reflects Flaws and Opportunities for Better U.S. Health Care," Commonwealth Fund, 2017, exhibit 2.

Given what we observe in the data, I see little, if any, basis for concluding that one of the two types of healthcare system works better than the other.

Transitioning

For the United States, transitioning to an insurance funds system would seem, at first glance, to be easier, because we could build on our existing employer-based provision of health insurance. But it would be no small matter. Insurers would need to shift from for-profit to nonprofit. Government would need to create a policy whereby the noninsured are assigned to an insurer or covered by a government program. Government would need to ensure that there is a basic plan that everyone can get. Prices paid to providers could be decided by negotiations between insurers, doctors, and hospitals, but government would need to be willing to step in and impose a decision if such negotiations fail to yield an agreement.

A transition to an American single-payer system could be done in one fell swoop, by expanding either Medicare or Medicaid to the entire population. Or it could be done gradually: lower the age at which Americans can get Medicare, raise the income limit for Medicaid eligibility, and add a Medicare-like program ("public option") that individuals and families can purchase on health insurance exchanges and that firms can purchase for their employees. Or simply allow any employer or individual to buy into Medicaid or Medicare, with subsidies for those who need them. Eventually, much of the population would be covered by these public programs. This would achieve universal coverage, and the government, as the dominant payer, would be in a strong position to control healthcare costs.3

- The following draws heavily from T.R. Reid, The Healing of America: A Global Quest for Better, Cheaper, Fairer Health Care,Penguin, 2009; Elias Mossialos, Ana Djordjevic, Robin Osborn, and Dana Sarnak, eds., International Profiles of Health Care Systems,Commonwealth Fund, 2017. ↩

- South Korea isn't included in the comparison here because it switched from one type of healthcare system to the other in 2000. ↩

- Jacob S. Hacker, "Stronger Policy, Stronger Politics," The American Prospect, 2016; Hacker, "The Road to Medicare for Everyone," The American Prospect, 2018; Dylan Matthews, "Donald Trump Promised 'Insurance for Everybody'. Here's How He Can Do It," Vox, 2016; Sarah Kliff and Ezra Klein, "The Lessons of Obamacare," Vox, 2017; Paul Starr, "The Next Progressive Health Agenda," The American Prospect, 2017; Starr, "A New Strategy for Health Care," The American Prospect, 2018; Michael S. Sparer, "Buying into Medicaid: A Viable Path for Universal Coverage," The American Prospect, 2018. ↩

-- via my feedly newsfeed

No comments:

Post a Comment