https://www.peoplesworld.org/article/harvest-of-discontent-trumps-trade-war-and-the-rural-fight-for-survival/

There is nothing normal about this September for farmers in the U.S. Midwest

Typically, at this midpoint in the month, farmers would be finishing up their small grains harvest and begin taking stock of other crops planted later in the season.

Harvest season this year, though, is well behind schedule.

The U.S. Department of Agriculture's September crop report, while slightly higher than the August estimates, shows corn and soybean yields are down from 2018 and lower than the projections shown in the last month's crop production report.

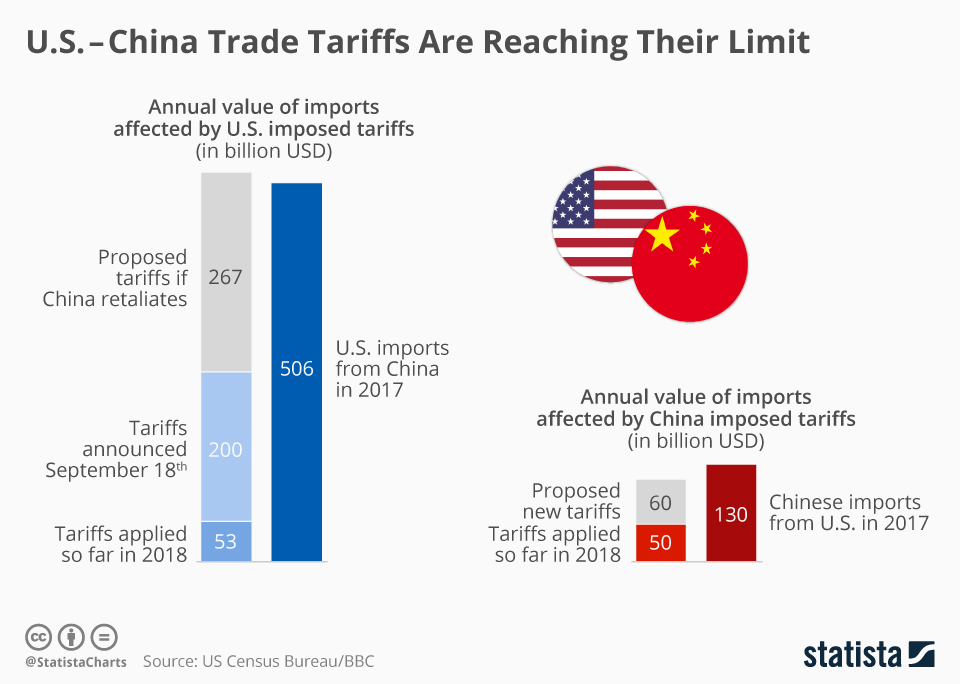

Chinese responses to U.S. tariffs have been substantive, but not proportional, so far. Here, the amounts of tariffs now in place and those threatened are shown. | U.S. Census Bureau and Stats.com

Chinese responses to U.S. tariffs have been substantive, but not proportional, so far. Here, the amounts of tariffs now in place and those threatened are shown. | U.S. Census Bureau and Stats.comAnd while yes, excessive spring rains and flooding across the Midwest can be blamed for delayed and prevented plantings, it's only one half of the issue.

For soybean farmers, in particular, their crop's supply and demand all depend on how the "Trump" card is played.

It's a high-stakes economic gambling match between the U.S. and China; a trade war fueled by the president's ego and a desire to contain growing Chinese power in the global economy.

The problems with political gambles like this one are simple and cruel: Human beings and their economic survival are the bargaining chips. And the "success" of such a strategy does not require a workable solution for all—just one side repeating the lie "We're winning!" while whittling away at peoples' livelihoods in pursuit of imperial ambition.

"We're tightening our belt, said farmer and president of the Iowa Farmers Union Aaron Lehman. "We're talking to our lenders, our landlords, and our input suppliers."

The IFU says its members are trying to cut costs any way they can just to make ends meet. The escalating trade war is their biggest concern now.

Instead of negotiating over trade disagreements, the U.S. has chosen "to insult our trade allies, pick all sorts of fights with our trade allies," said Lehman. "And then go to China and make outrageous demands that we knew were not going to be met."

A body blow to farmers and ranchers

For the last two years, the Trump administration has been in a tit-for-tat with the People's Republic of China, an ever-escalating battle of tariffs and import penalties. Trump has long accused China of unfair trading practices and intellectual property theft—actions which China of course disputes.

The fights over trade are episodes in a much bigger and longer-term campaign by the U.S.—no matter whether Republicans or Democrats are in power—to contain the growth of Chinese influence globally and maintain U.S. imperial dominance in East Asia.

Currently, the U.S. has hit China with tariffs on almost $550 billion worth of Chinese products, while China has hit back with tariffs on $185 billion worth of U.S. goods, primarily agricultural ones.

In a recent "gesture of goodwill," signaling the start of another ceasefire, Trump announced through Twitter the delay of a 5% tariff hike on another $250 billion worth of Chinese goods by two weeks—a departure from last month's plan to increase the tariff from 25% to 30%.

The gesture was not initiated by the Trump administration. The decision to delay followed China's decision to exempt more tariffs on 16 American products—fish meal, shrimp, and cancer treatment drugs, but did not spare the major goods subject to tariffs: soybeans and meat.

China did, however, buy $67 million worth of soybeans, but that's pennies compared to their $12.2 billion purchase in 2017.

These peaceful overtures come as the U.S. and China prepare to go back to the negotiation table in Washington in early October. Tensions remain high and substantial progress isn't likely, yet.

The lowering of crop prices, rainfall, and the trade war have created a perfect storm for farmers—leaving many without a roof over their heads.

"It already has driven some farmers off the farm, which not only hurts the farming community, but it hurts rural—small rural communities," said Gary Wertish president of the Minnesota Farmers Union. "It's been very devastating to rural America."

Farmers work to live, not to get rich.

They have high fixed costs, including the land they own, the tools and equipment, and the seed they need to grow crops. And while people can't control the weather, they can control the policies and tactics putting the squeeze on farmers and farm workers—it's a self-inflicted injury courtesy of the Trump administration.

How bad is it?

A report in July by the American Farm Bureau Federation revealed farm bankruptcy filings had risen by 13%. The report also found "the delinquency rates for commercial agricultural loans in both the real estate and non-real estate lending sectors are at a six-year high" and "above the historical average of 2.1 percent."

The Midwest and Southeast had the highest number of Chapter 12 farm bankruptcy filings. The Midwest is up from 215 filings in all of 2018 to 240 so far this year, a 12% increase. The biggest increase in bankruptcies, about 50%, happened in the Northwest, including Washington, Oregon, Idaho, Montana, and Wyoming.

"The deteriorating financial conditions for farmers and ranchers are a direct result of several years of low farm income, a low return on farm assets, mounting debt, more natural disasters, and the second year of retaliatory tariffs on many U.S. agricultural products," said Farm Bureau chief economist John Newton.

Newton also found that farm income should increase by 10% in 2019 from 2018, but those results would still be in the bottom quarter of annual results for the past 90 years. And the number includes direct payments from Trump's bailout package.

All roads, it seems, lead to a farm crisis not seen since the 1980s.

What about government aid?

Well, a cotton farmer in Texas gets $145 an acre for financial distress caused by the president. But a Minnesota farmer only gets $35 an acre for the hardest-hit crop.

"It makes no sense," said Betsy Jensen, the soybean farmer, in an interview with Reuters.

The payment discrepancies can be traced to the system set up to allocate the funds.

During the first round of bailouts, $12 billion total in 2018, farmers received money based on estimated lost sales by crop. Soybean farmers benefitted much more than others less impacted by the tariffs.

For the second round, payments are distributed based on the overall impact on agriculture in a particular county, and even with a rule preventing corporate farms from disproportionally benefiting from the plan, "the USDA's $16 billion bailout would still make rich farmers richer, thereby hurting small farmers," says the Environmental Working Group.

The National Farmers Union sees only one solution to this current crisis: "The president's erratic and destructive actions must end. All countries must be treated with respect and dignity and America's reputation as a reliable trading partner must be restored. Further, actions that have undermined the RFS must be rectified.

"Until these actions are corrected, and the markets rebound, we urge the administration to work with Congress to fundamentally reform and significantly strengthen the existing farm safety net."

Elections 2020: Candidates come courting

It's no secret rural voters helped elect Donald Trump in 2016.

Democratic presidential candidates are all pitching their solutions to the rural Midwest. Here, Sen. Bernie Sanders speaks at the Des Moines Register Soapbox during a visit to the Iowa State Fair, Aug. 11, 2019, in Des Moines, Iowa. | Charlie Neibergall / AP

Democratic presidential candidates are all pitching their solutions to the rural Midwest. Here, Sen. Bernie Sanders speaks at the Des Moines Register Soapbox during a visit to the Iowa State Fair, Aug. 11, 2019, in Des Moines, Iowa. | Charlie Neibergall / APHis campaign rhetoric of "being an outsider," focused on "draining the swamp and running the country like a business" resonated with a lot of rural voters.

They feel their communities are dying while their needs continue to be ignored.

Exit poll breakdowns from 2016 showed Trump winning between 65-70% of the vote in rural areas with populations less than 20,000, not near metro areas.

And despite the pain and further looming threats of financial and personal ruination caused by Trump's trade war, his presidential approval rating in rural areas is better than his nationwide standing.

Currently, Trump's favorable rating in rural areas is 55%, with 40% unfavorable in the nine states polled by a Change Research survey sponsored by the American Federation of Teachers and One Country Project, a rural voter outreach group.

The survey also found a plurality of rural voters, 39%, who said the trade war with China is hurting small towns in the short term, but it's necessary to restore a global trade balance. On the other side, 36% said the trade war is harmful in the short and long term, and it should be ended immediately.

"I am hearing from farmers in communities in North Dakota, and rural Americans across the United States, that the president's trade war is devastating their family farms and manufacturing communities—closing markets and leaving harvests to rot," said former North Dakota Senator and One Country Project founding board member Heidi Heitkamp. "Farmers are fed up, and I believe it is clear that rural Americans are looking for an alternative to Trump's failed leadership."

Democratic presidential hopefuls will need to learn from the mistakes of 2016 and do a better job addressing rural communities' common concerns and be able to talk to rural voters directly.

And as Democratic candidates begin flocking to Iowa to present their plans, there are signs that the large number of competing hopefuls in the primary may force them to pay attention to forging new connections to rural America. Candidates are eager to show they understand rural communities' economic pain; they're offering solutions and trying to show they are far removed from the preconceived notions rural voters have regarding the Democratic Party—and Republican Party for that matter, as distrust in both institutions was also seen in the Change Research survey.

"We cannot create an economy that works for all Americans if we continue to neglect the needs of rural America," Sen. Bernie Sanders said back in May during a visit to Osage, Iowa, going furthest in pointing out who some of the real enemies of small farmers are.

"In rural America, we are seeing giant agribusiness conglomerates extract as much wealth out of small communities as they can, while family farmers are going bankrupt and, in many cases, treated like modern-day indentured servants."

Meanwhile, it was just reported that fifteen members of Trump's 2016 campaign Agriculture and Rural Advisory Committee have collectively received over $2 million in trade war bailout payments. These payouts are among the billions of dollars that have flowed to owners of mega-farms rather than family farmers.

-- via my feedly newsfeed